Cloud Economics 2.0 – German Stock Exchange – Deutsche Börse – starts cloud computing exchange

We are entering the second wave of cloud computing: The Public Cloud Economics

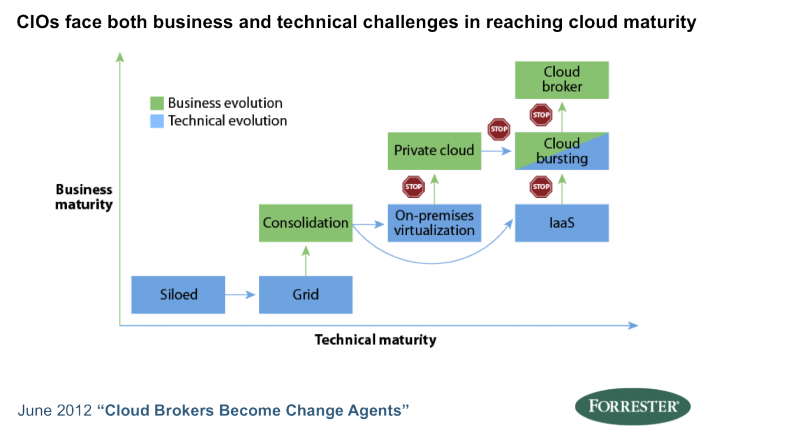

Most enterprises understand well cloud topologies (virtualization) and privacy levels (private, virtual-private, and public), or simply the different resource types (IaaS, PaaS, or SaaS). Some even embraced pretty sophisticated technologies like cloud bursting – the dynamic relocation of workloads. However, compared to this sophisticated understanding of technology, the understanding the current or even future economic models of cloud computing lags behind.

More than a year ago, Forrester introduced the corporate perspective of cloud economics with James Staten’s report Drive Savings And Profits With Cloud Economics. The major cloud providers surprised us also with many innovative business models, such as Amazon’s AWS Reserved Instance Marketplace last September. As an alternative to the fully flexible on-demand model, customers can also buy a one- or three-year contract for a compute instance and could save up to 60%. However, the risk is that you bought more than you need or simply the wrong instance types. The marketplace allows now selling off these half used contracts to other customers.

The variety of multiple different global cloud provider, local player, and even private cloud capacity, combined with different contract types such as the Amazon on-demand and reserved instance, stimulated the economic model of a cloud broker. See my reports about the cloud broker business model or the transformation process in larger enterprises.

While only very few large scape corporate IT divisions managed to establish a cloud broker style engagement model with their lines of business, quite some enterprises or government agencies use already external cloud brokers. This external service maps dynamically the demand to dynamic sourcing options. The state of Texas is for example using the cloud broker Gravitant.com across many state agencies.

With all the beauty of these new cloud economics, the perspective was still limited on the corporate resources or the selected resources of a specific cloud broker.

Until now!

But, this week’s announcement of the German Stock Exchange, Deutsche Börse, accelerated the cloud economics to the public level. They announced the plan to operationalize by Q1 2014 a public trading platform for infrastructure as service resources. The service focuses at the selling by cloud providers and buying by large enterprises or intermediates such as cloud brokers. While a cloud broker needs to understand many details of the certain customers such as workload classification, compliance requirements and even temporary on-premise spare capacity – the Deutsche Börse Cloud Exchange (DBCE) focus more on the trading similar to other resource trading marketplace services such as the electricity exchange or physical raw materials. It’s therefore more a sourcing channel for cloud brokers than a cloud broker on its own.

As I follow the space of cloud broker, cloud economics and cloud business models in general quite for some years now, let me allow two comments:

First of all, I’d like to congratulate the team at Deutsche Börse. Offering a public trading of cloud resources is really a courageous and bold move! It pushes the discussion of cloud economics to the level of public trading of long term capacity, spot capacity or even futures.

Secondly – and less enthusiastic – Deutsche Börse is just entering a steep learning curve and will most like realize the following limitations or challenges:

- Spot capacities are related to short notice sourcing. There have been other trails to crack this market such as spotcloud.com. Very likely the new DBCE needs to partner closely with selected cloud brokers who understand the real-time demand and get the actual IT supply chain operationalized.

- Long term contracts benefit less from a real-time exchange. The sourcing of three year contracts is more similar to B2B market place trading. Cloud providers will stick to the traditional B2B – RFP process.

- The DBCE demand will come from local cloud provider – not from enterprises. Many local cloud providers in Europe built an portfolio of own resources complemented by public cloud resources from the mega players, Amazon, Microsoft, HP, IBM, and Fujitsu. The DBCE will be an interesting sourcing option especially for these cloud providers that will simply resell public cloud resources to complement their portfolio of self-hosted services in Europe.

- Contract unifications matters! It was already announced today, but is one of the most challenging tasks. Ideally customers have only one existing frame-contract to all possible cloud providers on the DBCE. Unfortunately, the Germany law is very difficult and outdated in terms of IT contracts. The DBCE most likely has to cover the risk of the delivering cloud provider in the sense of a supply chain. (See also the German legal situation of a IT-Erfüllungsgehilfe). If DBCE manages to keep the right balance of unification and keep itself out of the contract relation it could work. Actually this concept is very similar to the alliances in the airline industry such as Star Alliance: unified purchasing, joint benefits such as mileage programs, but separate business units of each airline.

- Resell spare capacity of corporate data-centers is an illusion. Neither German data privacy laws, nor most cloud management stacks implemented in most private clouds would be able to share spare capacity to arbitrary external consumers brought in from the DBCE. However, if Deutsche Börse explores business opportunities around temporary spare capacities “subscribed” by European enterprises from public clouds. Some of this capacity might be up for sales and DBCE could become an independent counterpart to Amazon’s reserved instance marketplace.

- Industry (de-facto-) standards matter a lot. DBCE announced to use the german cloud management vendor Zimory to offer a light level of technical services. Zimory “manage” will be used for the buy-side integration, and Zimory connect will handle the sell side interface connecting to cloud providers. While Zimory has open APIs, it remains a proprietary cloud management solution. In contrast to this, DBCE must expect that a major part of cloud providers work on vmWare or already on the open source based OPENSTACK and will ask DBCE to use the same “stack”.

- It will only work for some workloads. IT departments or cloud brokers using a public cloud exchange basically speculate with capacity for these workloads that can be relocated easily. A forecasting calculation in the retail or financial services industry can be easily pushed to different locations every day, while a traditional ERP System will hardly change its location due to the huge data volume slowing down any movement.

- Enterprise will also transform their business models. The engagement model between IT departments and lines of business is changing to an OpEx model. Ideally the IT departments transforms from an cost center to a profit center, which enables them to cover the risk of under utilization or failed speculation at the exchange. Very likely we will even see the raise of a new wave of IT spin-offs stimulated by corporate cloud provider business models. However, Deutsche Börse needs to acknowledge, that this is a 5 to 10 year transformation requiring a long staying power.

Please leave a comment if you find the new offering by Deutsche Börse interesting.

Thanks

Stefan