Hindsight Is 20/20: Understanding The Rise Of Digital Customer Experience Platform

Smell that? That’s the smell of digital customer experience delivery technologies converging. Just kidding . . . but closer to the truth, you might be going deaf from the sheer volume of M&A and branding announcements over the past few years. Along with normal versioning announcements, 2013 held two key branding changes. Q1 witnessed Adobe’s shedding of the CQ moniker to adopt “Adobe Experience Manager” and cement its place among the expanding Adobe Marketing Cloud, and Q4 just witnessed salesforce.com’s debut of its “Salesforce1” customer platform.

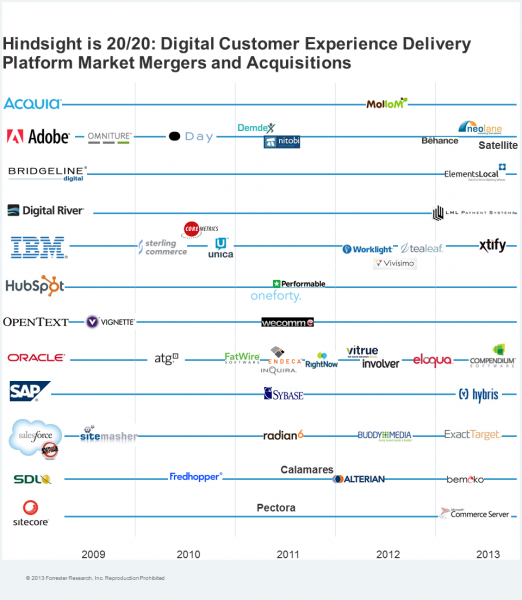

If you somehow tuned out all of the marketing/sensory overload, I’ll prove this to you another way. No peeking yet . . . OK, open your eyes! (see graphic).

Represented visually, it’s clear that M&A activity in the marketing automation space never even paused after Oracle purchased eloqua last holiday season: Salesforce bought ExactTarget in June, Adobe bought Neolane in July, and Oracle came back for seconds with its Compendium Software grab in October. Commerce continues its three-year hot streak: SAP grabbed hybris in June and Sitecore bought Commerce Server in November. Mobile and social haven’t completely lost their mojo either, as SDL picked up bemoko to further it’s mobile/omnichannel street cred and IBM hoovered up Xtify, a mobile messaging platform, in October.

You could shut your eyes to one or two of these events, but Forrester believes that this convergence trend is impossible to ignore as a whole — and it’s here to stay. Our latest report, Market Overview: Digital Customer Experience Delivery Platforms, demonstrates how some of these software vendors are doing more than branding and M&A announcements with tooling, runtime, and life-cycle integrations. Which of course, affects software buyers. Depending on your company, you’ll value different things, such as unified user interfaces from an integrated solution set served primarily from one vendor, or best-of-breed functionality via platforms sourced from multiple vendors (as long as they play nice together, AKA integrate smoothly).

We’re continuing our deep dive on this space, and we’d like your input. Specifically, how is your enterprise thinking about digital customer experience platforms? How is your enterprise quantifying integration? As business sponsors or IT leaders, what proof do you need to invest in a platform offering? Use the comments space below.