HCL Injects Innovation Into The Next Generation Of Product Development Services

In 2011, Forrester first reported on a new breed of mature and collaborative product development services (PDS) offerings coming to market, which we called “product development services 2.0.” These services are a stark contrast to traditional staff augmentation engagements. How are they different? Providers take greater responsibility for the end-to-end life cycle of the product, promise a higher level of industry and domain expertise, and offer a value-add service addressing key client business concerns. The transition has been gradual up to now, but there are finally signs of a more rapid shift.

One of the key announcements made in recent months was HCL’s launch of its “Service Line Unit” (SLU) initiative. Here are the key elements of this initiative:

• SLUs are a packaged set of PDS offerings, bringing together relevant HCL tools, partnerships, processes, and delivery competencies to address specific pain points.

• In developing these offerings, HCL systematically investigated the white space and the key business challenges in its chosen target markets. In turn, it invested in building out its own IP and domain knowledge to address these challenges.

• Ultimately, these investments and the targeting of specific business concerns will help HCL frame its service offerings in the context of key business outcomes, such as time-to-market.

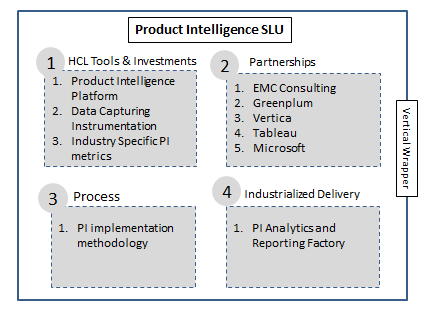

For example, HCL's product intelligence SLU seeks to enable organizations to take advantage of the vast quantities of data generated by products embedded with sensors or RFID chips. HCL has taken four key steps to develop this offering. It has developed:

1. Solution accelerators, such as its data capturing instrumentation.

2. Key partnerships — with leading business intelligence vendors, for example.

3. A sophisticated implementation methodology.

4. An industrialized delivery approach via its “analytics and reporting factory.”

HCL has already developed 25 such SLUs and aims to have approximately 40 within a year. Such an approach clearly requires significant upfront investment. Therefore, the shift to a more venture capitalist mindset is critical. Once those bets have been made, it is also critical to ensure the effective ongoing governance of these SLUs. HCL has put in place a product management team to define the road map for the SLUs.

Although it is not the best marketing term ever conceived, SLUs will ultimately enable HCL to differentiate on its domain and expertise, rather than its rate card. It injects much-needed innovation into this space and will provide critical differentiation from competitors still dominated by a staff augmentation approach. It unmistakably illustrates that the shift to product development services 2.0 is now underway — and will put competitors under pressure to accelerate similar initiatives.