Why Stripe’s Machine Payments Protocol Signals A Turning Point For Micropayments

For 30 years, micropayments failed for one reason: The payer was human. Humans hesitate; they abandon carts, resent friction, and perform mental accounting before every small transaction. The smartest engineers and best-funded companies in technology couldn’t engineer their way around human psychology — so they stopped trying.

On March 18, 2026, that constraint disappeared. Stripe and Tempo launched the Machine Payments Protocol (MPP) — and the entity doing the paying has no psychology to work around.

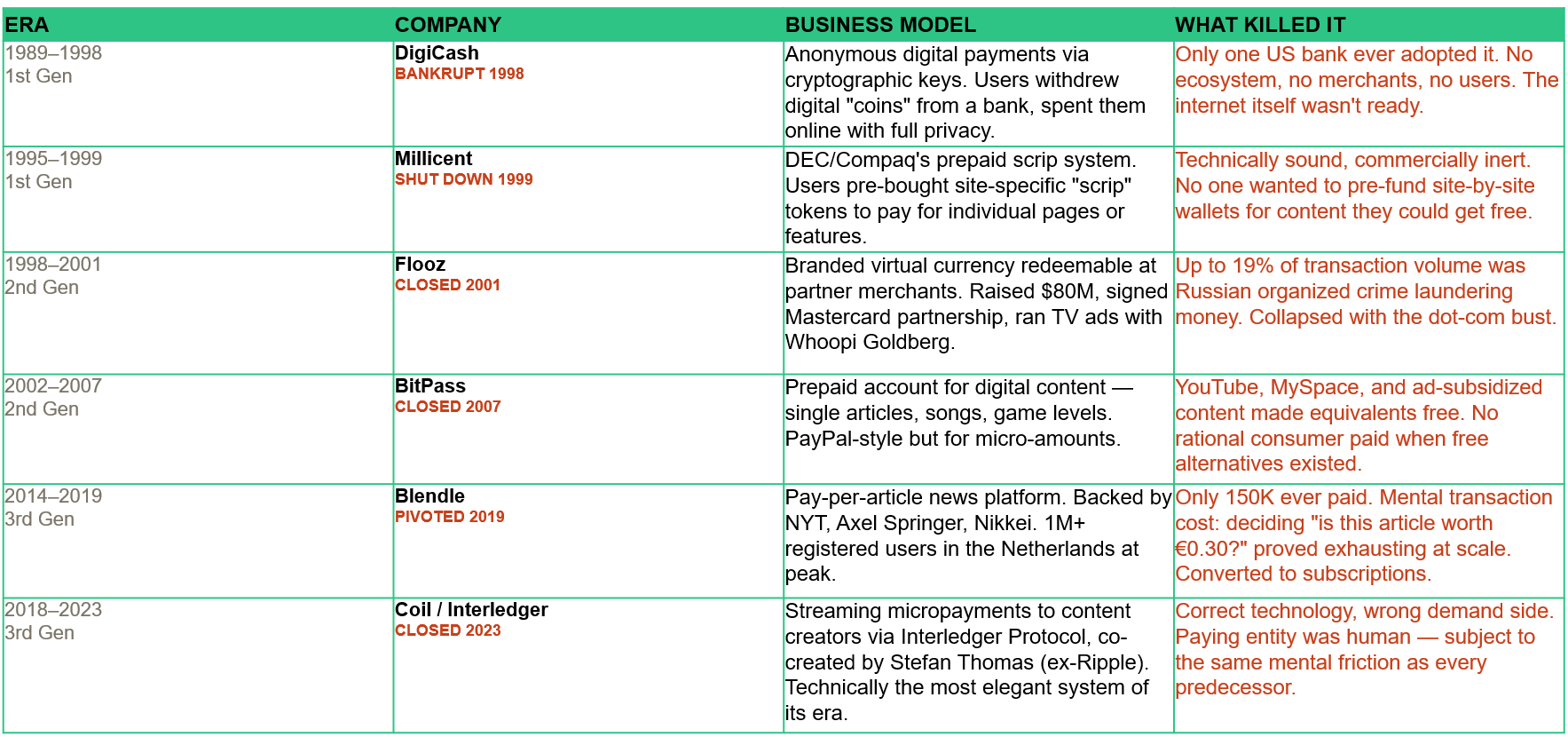

The Micropayments Graveyard: Three Generations Of Failure

To understand why the MPP matters, start with why everything before it failed. Below is a condensed history of the most significant attempts — organized by generation, each dying of a different cause.

The 30-year history of micropayments

The 30-year history of micropayments

The pattern across all three generations is identical: Every attempt assumed that the paying entity was a person. The Machine Payments Protocol is the first protocol built for an entity with no psychology to navigate.

Why The MPP Is Structurally Different

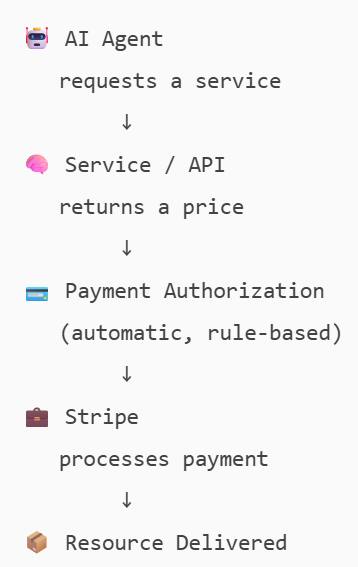

Stripe and Tempo launched the MPP alongside the Tempo Mainnet — a payments-focused blockchain codeveloped with Paradigm. But one design principle separates it from everything above: The MPP is built for agents to pay — not humans. Unlike every prior micropayment system, no human decision point exists between resource request and payment execution. Payment becomes a programmatic step, not a conscious decision.

The MPP payment flow

This solves the 30-year problem at its root. AI agents have no mental transaction cost, they don’t hesitate before paying $0.001 for an API call, and they don’t abandon carts. They simply execute payment as a function call and continue with the task.

Machine‑initiated payment models invert this assumption. They’re designed for nonhuman actors — such as AI agents, automated workflows, and software services — that need to pay for resources like data access, compute, APIs, or digital services in real time.

From an architectural standpoint, protocols like the MPP embed payment directly into the request‑response cycle between an agent and a service. Payment becomes a programmatic step, not a discrete decision. There’s no “checkout moment,” no cart abandonment risk, and no mental transaction cost.

This is consistent with Forrester’s broader research on agentic AI, where autonomous systems increasingly operate across procurement, finance operations, software development, and customer engagement. As agents take on more end‑to‑end responsibility, they require the ability to transact independently — within predefined controls.

Three structural shifts make this approach more viable than previous micropayment efforts:

- Payment is a prerequisite, not a preference. Unlike human consumers, agents can’t substitute free alternatives when a required service is unavailable. If a workflow depends on a specific dataset or API, payment is mandatory for task completion. This eliminates one of the biggest adoption barriers that undermined earlier models.

- The payments infrastructure is already in place. Unlike past experiments that required new wallets, browser extensions, or proprietary networks, current approaches are designed to operate on top of existing card rails, bank transfers, and — increasingly — tokenized money.

- Enterprise use cases lead adoption. Initial demand is coming from enterprise and developer environments, not consumer content. This mirrors Forrester’s predictions in B2B payments, where automation, reconciliation, and straight‑through processing drive willingness to pay — even for small, frequent transactions.

An Emerging Stack, Not A Single Winner

One common misconception is that machine‑initiated payments will converge on a single dominant platform. Forrester’s view is the opposite. The emerging ecosystem already spans multiple layers, such as:

- Protocol and standards. These define how agents request services and trigger payments. Besides Stripe’s MPP, we also see Coinbase’s x402 protocol, which activates HTTP 402 for instant USDC payments directly over HTTP with zero protocol fees, sub-2-second settlement, and crypto-native path. Two ex-Stripe engineers also founded Circuit & Chisel, which introduced the Agent Transaction Protocol, helping AI agents navigate the web and execute payments as part of multistep task completion.

- Identity and trust frameworks. These address the question of “Who’s this agent?” — a theme closely aligned with Forrester’s research on AI agent identity management, Zero Trust, and fraud management for AI agents. Silicon Valley agentic payments startup Skyfire introduced the Know Your Agent (KYA) protocol using JSON Web Tokens, which gives AI agents a verifiable identity so merchants can distinguish legitimate agents from malicious bots — and accept payment from verified ones. KYAPay supports agent-to-agent, B2A, and A2B payments both on-chain and off. Skyfire recently formed a strategic partnership with F5 to enable enterprises to securely enable verified AI agents while still blocking malicious actors.

- Wallets and programmable controls. These enable spend limits, policy enforcement, and auditability. Blockchain wallet infrastructure provider Crossmint gives AI agents their own wallets, virtual Visa/Mastercard cards, and stablecoin accounts with programmable spending controls, such as per-transaction limits, merchant whitelists, and human approval thresholds. It’s protocol-agnostic and supports both x402 and card rails.

This mirrors the evolution of the internet itself: interoperable layers rather than a winner‑takes‑all model. For banks and payment companies, this creates both opportunity and risk. Value will accrue unevenly across layers, and late entrants may find key control points already claimed.

Implications For Banks And Payment Companies

Financial institutions face a narrowing window. Those that wait for transaction volumes to materialize will find the identity, trust, and wallet layers already owned by fintechs, card networks, and crypto infrastructure providers. Three strategic options remain open — for now:

- Become a trust and identity anchor for agent‑initiated payments. This extends existing know-your-customer and risk capabilities to nonhuman actors

- Provide compliance and cross‑border controls. This is especially important as agents begin to transact autonomously across jurisdictions — a growing concern in markets like Asia Pacific with fragmented regulatory regimes.

- Develop agent‑native financial products. This includes usage‑based settlement accounts, real‑time treasury visibility, and agent‑specific fraud monitoring.

Final Thoughts

Micropayments didn’t fail because the industry lacked imagination or engineering talent. They failed because the assumed payer — a human — was wrong. Machine-initiated payments remove that assumption permanently. The most important question for financial institutions is no longer whether this works — it’s whether they move before the control points are claimed. That shift is already underway.

Forrester clients can set up an inquiry or guidance session to discuss these topics with us. We will also publish new research around agentic payments soon. Stay tuned!

Categories