Be In The Know: The Managed Service Provider Journey

Over the last two months, I’ve had the opportunity to interview a plethora of managed service providers (MSPs) and MSP platform vendors across the US, Europe, and Asia. The experience has provided me with an inside view into the fastest-growing technology channel today, but it has also provided me with a clear understanding of the evolutionary path MSPs must take as they attempt to reach a new level of maturity (and profitability).

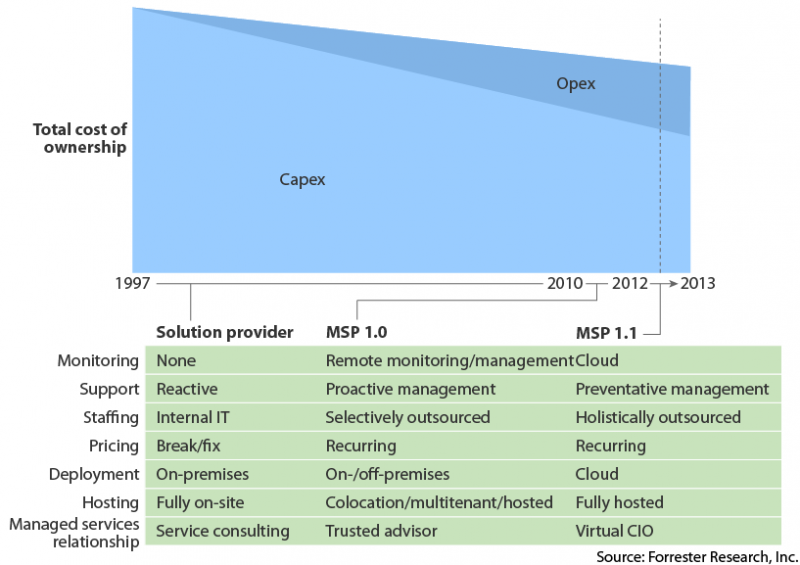

For those tech vendors hoping to cash in on the budding billion-dollar managed service opportunity, it is critical to first understand where the movement began in order to understand where it is headed. The figure below (from my most recent report, Managed Service Providers, Part 1) highlights the three unique stages of MSP development:

- Past (pre-1997): solution provider model. Up until the end of the 1990s, SMBs employed their own internal IT systems, supported by a small IT staff or local consultant. They purchased from and had their IT systems installed by VARs, and got their phone systems from telecommunications providers. An IT solution provider (most often the VAR or consultant) provided reactive break-fix support and maintenance for their hardware and software. For SMBs, this model represented a heavy capital investment (capex) for their IT systems and a heavy operating expense (opex) for labor, all executed on-site.

- Present (1997 to 2011): managed service provider model (MSP 1.0). In the late 1990s, a revolution occurred for solution providers: A disruptive software category called RMM (remote management & monitoring) hit the market, and SMBs started to outsource specific IT administration and support functions under a new business model — managed services. This model enabled MSPs to achieve enhanced efficiency, cost savings, and elastic scalability by providing one-to-many IT support services on a proactive, remote basis. It offered big opex savings for customers and recurring revenue streams for themselves.

- Future (2012 onward): managed service provider plus cloud model (MSP 1.1). Cloud computing enables the delivery of integrated managed and hosted resource services. In this model, premise-based IT systems become centralized and virtualized to create greater operational efficiency and reduced capex for customers. Similar to MSP 1.0, the MSP 1.1 model involves a deployment fee and a monthly recurring services fee.

This new aspect of MSPs’ business model, MSP 1.1, is the future of the MSP industry and is having significant impact on the MSP landscape. Whereas the first two stages primarily focused on IT infrastructure, the MSP 1.1 model fully merges IT infrastructure with other cloud services (e.g., storage, application hosting), making it a technologically stronger spawn of the MSP 1.0 model. I believe, over time, that this evolutionary next step is required for MSPs to maintain their growth and viability.

Please share your thoughts and/or questions!