Asia Pacific Online Video Advertising Spend Will Reach $53.7 Billion By 2023

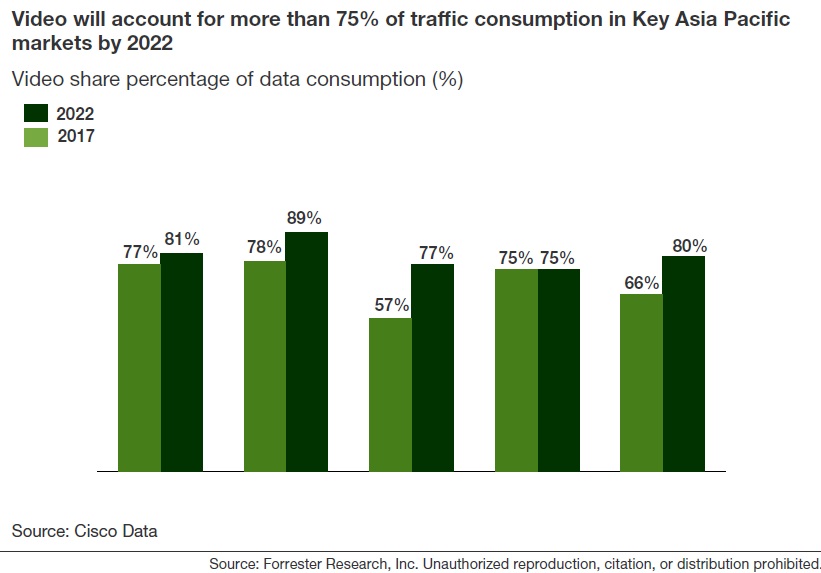

Increasing internet penetration, better data infrastructure, and increasing adoption of 4G and now 5G are driving video consumption in Asia Pacific. The Asia Pacific region is a mix of heterogeneous markets such as Australia, Japan, South Korea, China, and India. Markets like South Korea and China are leading globally in term of 5G adoption, and markets like India and, again, China have a huge potential in terms of new users joining the internet every day and low revenue per capita, which is expected to increase in coming years. As per Cisco, online video consumption is set to more than triple in key Asia Pacific markets between 2017 and 2022, and India will witness the fastest growth. Not only will video be the fastest–growing medium, but it also will account for the majority of data consumption. As a result, we expect that Asia Pacific online video advertising spend will reach $53.7 billion by 2023. You can read more about the Asia Pacific online video advertising landscape in detail in our latest report, “Forrester Analytics: Online Video Forecast, 2018 To 2023 (Asia Pacific).”

Forrester divides online video into two categories: display video and social video. Display makes up a larger part of online video advertising spend, given the higher contribution from in-stream video, but we expect display video’s share to decline with the increasing influence of social video.

- Display video includes in-stream video, video advertisement on eCommerce, news websites, etc. In-stream video apps such as YouTube account for the lion’s share of display video advertisement revenue, with multiple options to monetize their user base via pre-/mid-/post-roll advertisement.

-

- Display video advertising growth has been slowing down in recent times, as they’re being cannibalized by their own subscription service as well as the increasing popularity of short video apps, especially in China. Not all markets have shown this downward trend, as ad-supported in-stream video services are still doing well in some APAC countries such as India.

- Social video is more of a newbie to the online video space. Key social players were late in adding video products, but now they’re aggressively focusing on it; Facebook, for example, has added new products like Stories and Watch. We expect video to account for a higher share of social revenue in coming times.

-

- Short video apps such as TikTok and Kuaishou gained popularity in 2018 and are expected to play a bigger role in APAC’s social landscape. Short video apps are an engaging and cheaper medium to reach younger consumers, and brands have started trusting and investing money in them. As a result, 2018 has been an exciting year for short video players, and Forrester expects that they will account for 5% of APAC digital marketing spend in 2019. You can read more about short video apps and their influence on Asia Pacific’s digital landscape in our latest report, “TikTok Excels In The Age Of Short Videos.”

Note

Display video: Display video advertising includes video banners, other streaming ads, pre-/mid-/post-roll ads, and in-text video but does not include YouTube overlay ads. It includes video ads that run in conjunction with internet-based streaming video content consumed on PCs, tablets, smartphones, and connected TVs or TV devices. This includes streaming online video that is supported by advertising like OTT, online video consumed on a website or app, and video used by eCommerce players in online marketing services.

Social video: Social video advertising targets social video users as well as general social media users. Given the various types of social video ads, a user can see a social video ad without necessarily being a social video user.