Which Technology Service Providers Are Strategic To The Enterprise?

For the first time, we reveal what 2,078 enterprise services decision-makers have to say about their strategic partners. But first, some groundwork.

After a reset in revenue expectations last year, service providers are back on a slow growth trajectory. Why? Because companies need more help than ever. Services are a huge part of most IT budgets. Forrester’s tech forecast projects that firms will spend $1.6 trillion dollars on services globally by 2028. For many firms, that’s almost a third of the overall IT budget. Based on Forrester’s most recent survey of 2,078 enterprise services decision-makers, my colleague Ben Nagle and I dove into the data to identify three trends that define the year:

- A continued pivot towards results-based pricing models. The bell tolls for time-and-materials pricing. More than half of services decision-makers use outcome-based pricing, and 46% use fixed-price contracts.

- More demands for more kinds of assistance, particularly from strategic partners. We track 12 categories of service in this dataset, from consulting and business app implementation to security, engineering, and AI services. Across the board, enterprises expect to spend more on services next year in all these categories, often led by the disruptive impact of AI. Forrester clients can reach out to dive into the details of each category.

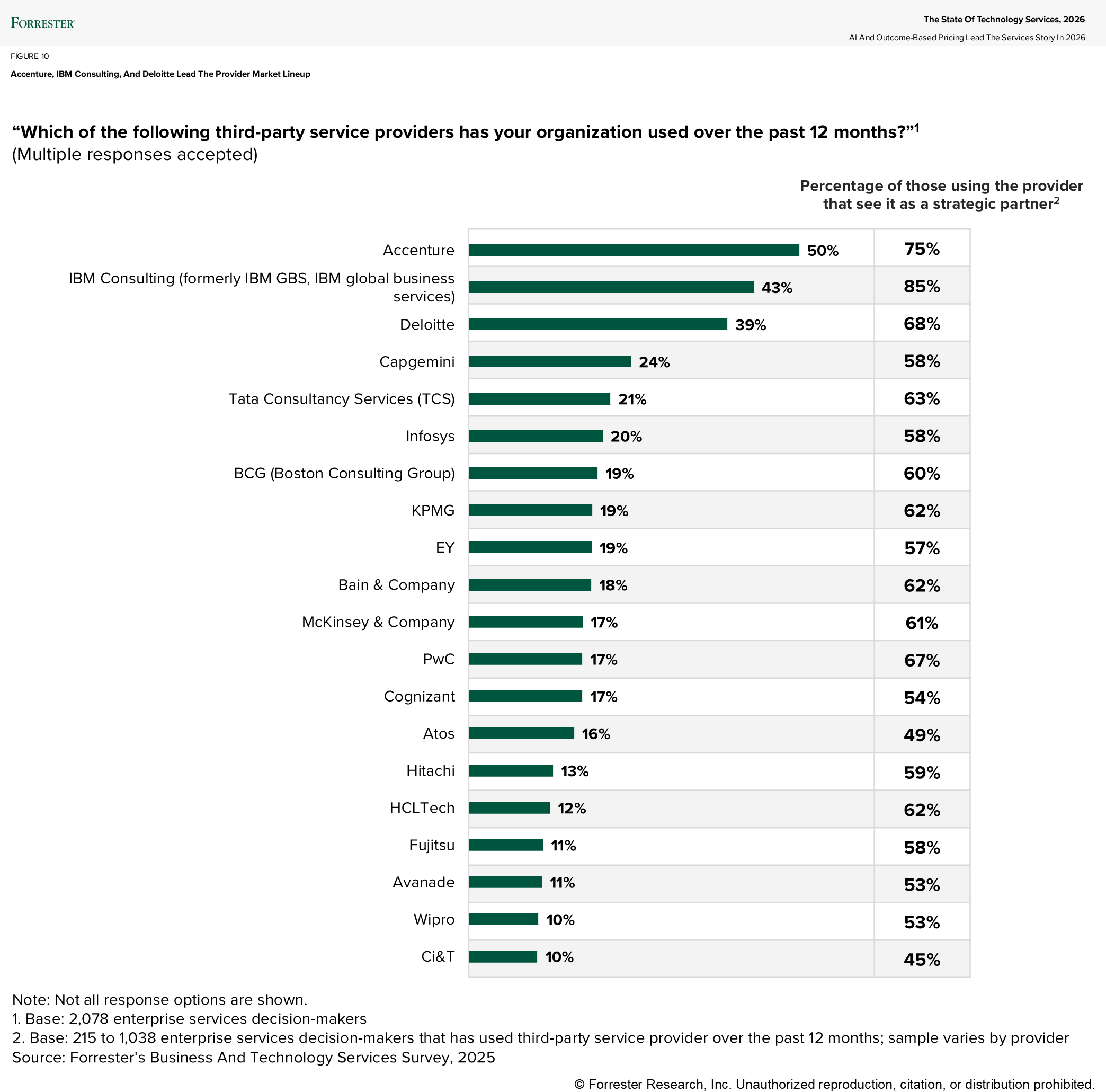

- A clear market dominance by the largest providers. This survey reveals the enterprise adoption levels of service providers and the percentage of each brand that buyers see as strategic partners (see the figure below). Two results stand out: 1) Accenture, IBM, and Deloitte lead the market in adoption and 2) might doesn’t always make right. Smaller providers such as Bain sometimes outpace their direct competitors. Less commonly adopted providers like PwC can have higher strategic partner ratios.

Invest More In And Expect More From Your Strategic Partners

The survey asks services decision-makers about the providers they use and which they see as strategic. We go into details for 34 providers, asking questions that highlight the value they bring, where respondents are satisfied or dissatisfied, where they face challenges or receive benefits and, overall, what matters when viewing a provider as a strategic partner. We found that:

- Relationships — not commercial terms — define strategic partnerships. Enterprise respondents most often cite industry or domain expertise, with 55% using those factors to define when a provider is a strategic partner. Twenty-nine percent of respondents value trust and experience with the provider, and 22% value strategic partners’ investment to cocreate and co-innovate with them.

- Capabilities are the baseline, starting with technology expertise and program execution. To be a strategic supplier, a provider must of course bring technology expertise — 32% of enterprise respondents prioritize this factor — and the ability to handle projects end to end, as 22% demand. For a technology leader, be sure to bird-dog the quality of your provider teams and insist on improvements via a conversation, not a cudgel. If they do not respond quickly with an improved team, are they truly a strategic partner?

- Buying networks make better provider choices. Forrester’s data shows that an average of 16 internal stakeholders and nine external participants influence purchasing decisions. Larger buying groups bring higher confidence, despite more decision complexity. When we asked buyers with an internal buying group size of six or more people about the impact of larger buying groups (i.e., six or more internal participants), 93% reported clear benefits: broader perspectives, shared effort in validating solutions, lower risk of making poor choices, better ability to secure budget, or greater likelihood of approval.

Strategic Partnerships Require More Than Scale — But It Doesn’t Hurt To Be A Giant

Categories