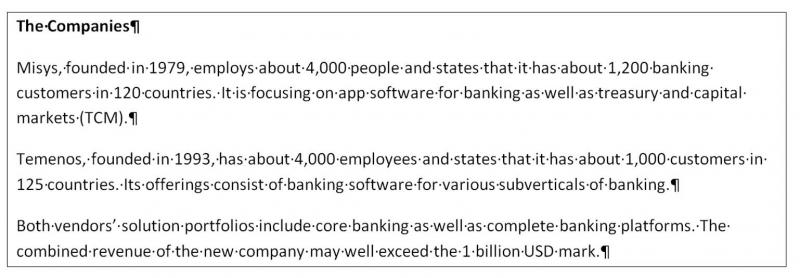

The Merger Of Misys And Temenos — Moving Out Of The Gap Between Gorillas And Antelopes

Less than a week ago, initial information became public that Misys and Temenos may intend to merge. On February 7, 2012, a press release stated that “Temenos and Misys today confirm that they have reached agreement in principle on certain key terms and are in continuing discussions regarding a possible all share merger of the two groups.“ Now Misys and Temenos have about one month to finalize their merger — or abandon it. It is obvious that this merger has the ingredients to become one of the most significant mergers in the banking industry in the past few years. With the probability of the merger now sufficiently high, here is my initial take.

There are two obvious reasons for this potential endeavor of Temenos and Misys (let’s call the combined company MIsys-TemeNOS [“MiNos”] for the time being to avoid terms such as “new company” or “NewCo”):

- A broader and deeper product portfolio for banking and capital markets. While Temenos has been a Global Power Seller in Forrester’s global banking platform deals survey for years, Temenos has so far struggled to win a large number of major banks as customers for its banking platform. The combined portfolio could make “MiNos” more attractive for larger as well as smaller potential customers — with an even broader set of point solutions as well as integrated apps offerings such as banking platforms.

- A truly large banking software company. “MiNos” will leave the challenging space between the large powerful gorillas and the tiny fast antelopes — putting “MiNos” in a more powerful position to compete with its larger competitors in the business apps space such as Oracle and SAP as well as vendors with combined banking platform/services offerings such as Infosys and TCS.

However, there are also a number of risk factors:

- Overlap in the two product portfolios: The new portfolio will consist of both complimentary and redundant software products. Official statements (as far as statements can be official at this stage) say that “MiNos” is committed to maintaining and developing Temenos T24, Misys BankFusion, as well as the Misys TCM portfolio. Does this commitment to multiple banking platforms make economical sense — particularly in the long term? What will happen with the remaining, in some cases conflicting, solutions? Let’s use lending as an example: Misys LoanIQ is more mature and maybe functionally richer, while the related Temenos T24 module is more modern and already pretty successful.

- Integration architecture: Even today, Misys may propose nine or ten Misys solutions (plus third-party apps) to cope with the needs of a small to medium-size bank, while Temenos will likely offer a smaller number of solutions. In a combined product portfolio, this heterogeneity will be multiplied by heterogeneous application architectures —between the Misys and Temenos portfolios and particularly also within the Misys portfolio. “MiNos” will quickly need to design an integration architecture/framework (which could nicely be based on the best conceptual elements of BankFusion’s architecture) to avoid perception of the combined solution portfolio as “yet another bunch of nonintegrated banking applications.”

- Different corporate cultures: Knowing both Misys and Temenos, I dare say that the corporate cultures of the two firms are not entirely compatible. This is particularly relevant when it comes to retaining key corporate staff in a situation like this (coincidental or not: Misys CEO Mike Lawrie will move to CSC in a few weeks). However, there is more. To use the wording of an email from South America that I received shortly before starting to write this blog post: Misys and Temenos have been “almost mortal enemies” in the core banking/banking platform space for years. Can the sales forces of those “mortal enemies” be convinced to work toward a common goal?

- Customer perception: Even right now, with no details regarding the shape of, for example, the new company, its future product portfolio and targeted customer segments, early client feedback ranges from “deeply worried” to “slightly enthusiastic.” This is not unusual. However, it is unusual that “MiNos” will need to cope with a thousand and maybe even close to two thousand customer firms that might see investment supporting the core business at risk. It will be up to “MiNos” to succeed in helping its customers in mitigating (maybe perceived) merger risk. And it will need to do this fast to avoid losing in multiple ongoing bid processes.

Right now, it is way too early to judge whether the (at this time still potential) merger will become a success. There are way more questions than answers. It is obvious that “MiNos” will need to define and communicate concrete road maps for the joint product portfolio to retain its existing customers and avoid any perception of risk as far as the future of the individual solutions — and thus also targeted customer groups — are concerned. Both companies are very experienced in integrating acquired companies. However, this may be exactly the risk when it comes to a merger of shares between two firms of comparable size and standing.

If you are currently working on selecting a new banking platform for your bank, watch the ongoing developments carefully to be in a good position to mitigate selection risk. Do you see the merger as a benefit or a risk for your ongoing projects — in terms of, for example, targeted customer groups, your solution portfolio and road map, available functionality, solution architecture, and well-tuned delivery capability? As always, I am interested in what you think: JHoppermann@Forrester.com