The State Of Stablecoin In Japan

In a recent conversation with Makoto Shibata (Head of FINOLAB and former managing director and head of the global innovation team at MUFG), I explored how stablecoins are evolving from crypto experiments into real financial infrastructure in Japan. The takeaway? Japan’s stablecoin ecosystem is no longer just living in paper and pilot. It’s real, regulated, and rapidly expanding.

From Prepaid Tokens To Regulated Stablecoins

Japan’s stablecoin journey began with JPYC Inc., which issued the first regulated yen-pegged stablecoin, JPYC, in Japan in October 2025. JPYC Inc. is also a FINOLAB-incubated startup that launched the country’s first yen-pegged digital token in 2021. At the time, Japan lacked a legal framework for stablecoins, so JPYC operated as a prepaid payment instrument — essentially a digital gift card that could be purchased with yen but not redeemed for cash.

That changed in 2023 when Japan’s revised Payment Services Act introduced a regulatory framework for fiat-backed stablecoins. By 2025, JPYC had transitioned into a fully licensed electronic payment instrument, enabling one-to-one redemption with Japanese yen. As Shibata-san explained, “They started with a work-around, but once the regulation was in place, JPYC became the first regulated yen stablecoin in Japan. That was a major milestone.”

Today, JPYC operates under a Type II funds transfer license, with a ¥1 million (~US$6,700) daily issuance and redemption cap per user. The Japanese stablecoin issuer aims for an ambitious 10 trillion JPYC (US$65 billion) in circulation within three years of its October 2025 launch.

Why It Matters

Stablecoins are solving real-world problems in Japan: high remittance fees, slow cross-border settlements, and costly merchant payments. With the Bank of Japan raising interest rates for the first time in decades, stablecoin issuers now have a viable business model — and regulators are giving them room to grow.

What’s Happening

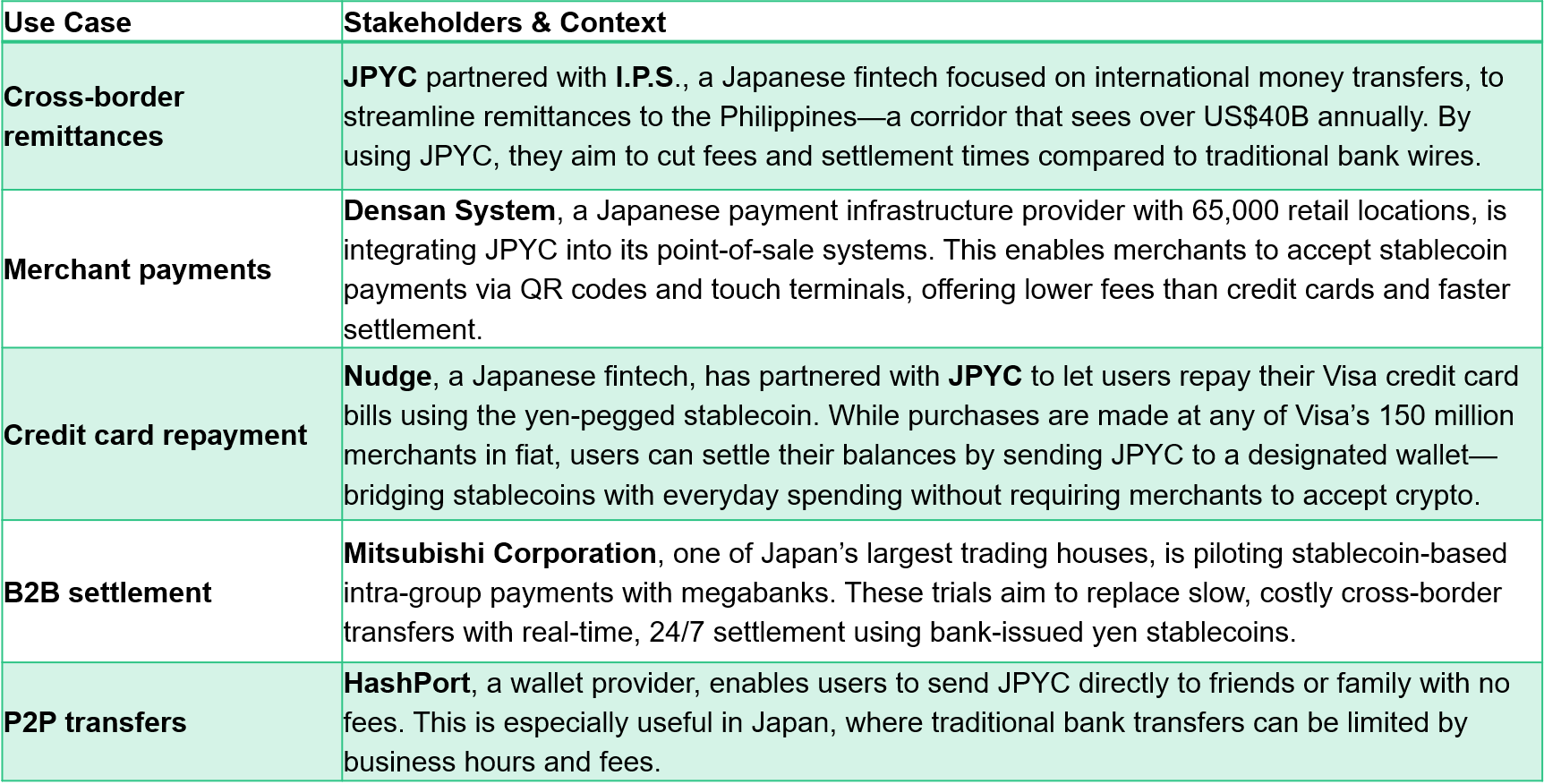

- JPYC is already used for peer-to-peer transfers, merchant payments, and even credit card spending.

- Japan’s three megabanks, MUFG, SMBC, and Mizuho, are piloting bank-issued stablecoins for B2B and cross-border use, targeting ¥1 trillion (~US$6.5 billion) in issuance by 2028.

- Wallet providers (e.g., HashPort), payment integrators (e.g., Densan System), and exchanges (e.g., SBI VC Trade) are building the stablecoin rails for adoption.

As Shibata-san put it: “Stablecoins are not speculative assets in Japan — they’re becoming financial infrastructure.”

Where It’s Working

What To Watch

- Licensing limits: JPYC’s ¥1 million/day (~US$6,700) cap restricts large transactions. A Type I license would unlock broader use.

- Interoperability: Multiple yen stablecoins are emerging. Seamless exchange between them is critical.

- Ecosystem integration: Payment gateways, wallets, and exchanges must align to drive adoption.

- Bank moves: Megabanks are still in pilot mode. Their entry could mainstream stablecoins if they move fast.

What Banks And Payment Providers In Other Developed APAC Markets Can Learn

Japan’s stablecoin rollout offers valuable lessons for financial institutions and fintechs across developed APAC markets:

- Singapore: With a mature real-time payments infrastructure (e.g., FAST, PayNow), stablecoins may not solve for domestic transfers, but they could unlock new models for programmable payments, cross-border remittances, cross-border B2B settlement, and tokenized loyalty ecosystems. Japan’s use of stablecoins for credit card repayment and merchant payments offers a blueprint for integrating digital assets into existing rails.

- Hong Kong: As the city accelerates its e-HKD pilot and explores stablecoin regulation, Japan’s regulatory clarity and phased rollout of JPYC provide a practical reference. The use of stablecoins for real-world commerce, without requiring merchants to handle crypto, could help Hong Kong bridge its digital asset ambitions with its traditional financial sector.

- Taiwan: With a strong fintech ecosystem and growing interest in digital currency innovation, Taiwan can look to Japan’s model for how to incubate stablecoin startups (e.g., FINOLAB’s role with JPYC), align with regulators early, and focus on real-world use cases such as remittances and small-/medium-sized enterprise payments.

- Australia: As the Reserve Bank of Australia explores central bank digital currency pilots and the Treasury develops a regulatory framework for digital assets, Japan’s experience shows how private-sector stablecoins can complement public initiatives. The Nudge-JPYC model demonstrates how fintechs can extend the utility of stablecoins through traditional credit card and retail payment integrations.

Across these markets, the key takeaway is that stablecoins don’t need to replace existing systems — rather, they can enhance them. By embedding stablecoins into familiar interfaces such as credit cards and merchant networks, Japan is showing how to make digital assets usable, compliant, and consumer-friendly.

What To Read Next

Forrester has dedicated research and blog posts on payments innovation such as stablecoin-based payments and B2B cross-border payments, including:

Mastercard Makes Its Stablecoin Move: The BVNK Acquisition

How Stripe And Bridge Are Pushing Stablecoin Real-World Adoption: A Conversation With Mai Leduc

Ant International’s Playbook On AI, Blockchain, And Wallet Network

Predictions 2026: Asia Pacific

The Cross-Border Payment Solutions For B2B Landscape, Q1 2024

Forrester clients can set up an inquiry or guidance session to discuss these topics with me.

Categories