Forecasting In Uncertainty: Why Scenario A Is Looking More Likely For Some Countries And Scenario B More Likely For Others

Last week, the International Monetary Fund (IMF) issued its April World Economic Outlook report. The headline was that the world’s real GDP would fall by 3% in 2020, which is a much steeper drop than in the 2008–2009 recession. For the purpose of projecting the tech market outlook, the more important numbers are real GDP forecasts for individual countries. The IMF projected that real GDP for the US would drop by 5.9%, for Euro countries 7.5%, for Japan 5.2%, for Canada 6.2%, and for Eastern Europe and Latin America 5.2%. China’s and India’s economies would grow but very slowly, less than 2%. For 2021, the IMF projected good rebounds in economic activity, with real GDP for advanced economies averaging 4.5% growth. But the IMF added a major caution to these forecasts: “The risks for even more severe outcomes, however, are substantial.”

As I’ve noted in prior blog posts, we are working with two primary scenarios for the economic/tech market outlook. Scenario A assumes a relatively short but sharp two-quarter recession in 2020, with growth resuming in 2021. Scenario B assumes the recession lasts into 2021 as pandemic containment efforts slowly ease back or recur if COVID-19 resurfaces or stubbornly persists. The IMF forecasts provide the economic underpinnings for our tech market forecasts in Scenario A. But we continue to provide tech market forecasts under Scenario B, reserving the fact that under this scenario, an economic downturn as long as the Great Depression is a remote possibility.

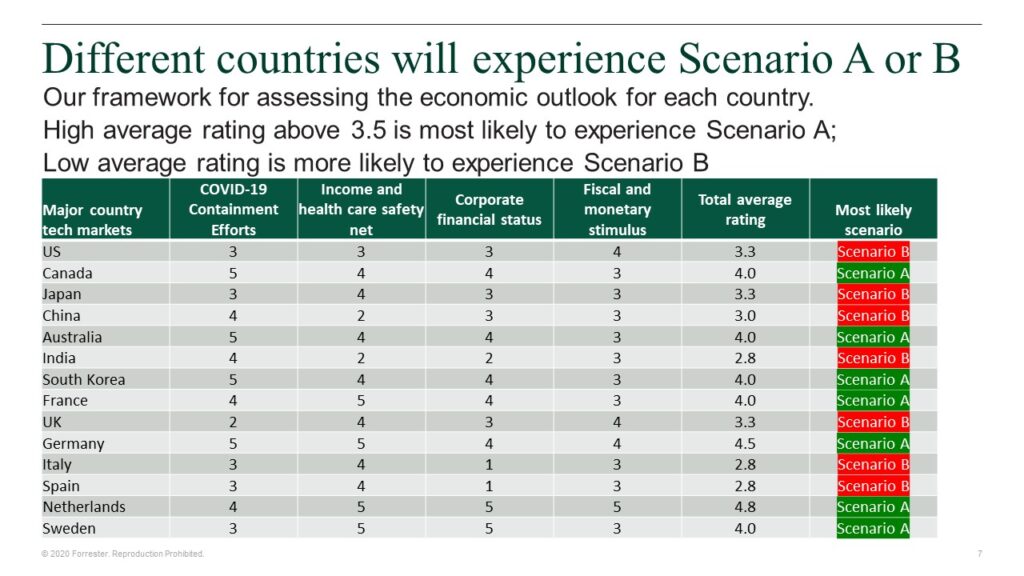

The real question is which will be more likely: the Scenario A tech market forecast or Scenario B projection? To answer that question on a country-by-country basis, I have created a four-factor model to assess the probabilities for each scenario:

- Timing and effectiveness of COVID-19 containment efforts. China or South Korea, which moved quickly to impose containment efforts — including extensive testing — stand a better chance of a relatively short economic downturn and relatively quick recovery. China is at risk, however, of slipping back if it is true that it is downplaying the signs that the virus is returning. Germany and the Netherlands were a bit slower to get started but have had good success keeping down hospitalization and death rates. Countries such as the US, Italy, Japan, Spain, and the UK that were slower to act and did so unevenly will have a slower recovery path. This factor will remain important because of the prospect that the virus can flare up again, as is happening in Singapore and China. How well a country handled the first encounter with COVID-19 gives some guidance on how well it will handle a second or third.

- Strength of health and income security underpinning consumer confidence. Consumer confidence will help determine whether consumers return to their spending patterns before the recession or remain shell-shocked and hypercautious. European countries with broad income support programs will keep consumers from losing too much income during the downturn, thus allowing them to start spending as containment policies scale back. Similarly, consumers in these and other countries with universal health care insurance, such as Italy, Spain, Australia, and Canada, will be less worried about medical bills related to COVID-19 treatments. In contrast, the US’s social safety net has been geared toward the elderly and its health insurance system oriented toward those employed. That has left many low- or middle-income US households exposed to layoffs or furloughs. As a result, US consumers may want to concentrate on savings to avoid being caught short and will hesitate to buy a new car, home, or go on vacation.

- Financial positions of businesses in each country and their ability to resume investment. Warren Buffett once famously said, “Only when the tide goes out do you discover who’s been swimming naked.” This recession has shown that many companies were operating with weak balance sheets, high debts, and thin reserves of cash and marketable securities. When business starts to pick up as pandemic lockdowns ease, companies in this position will focus on paying down debts and rebuilding cash positions, not making big new investments. Across all industries in the US, the debt-to-equity ratio is over 1.o in 2019 from .64 in 2014 (see the ReadyRatios website). Shale-oil companies, department stores, apparel retailers, airlines, and auto dealers are especially vulnerable; all have been hard hit by COVID-19 lockdowns. Other countries like Italy and Spain have their own industry sectors with strained financials. But in countries like Germany, the Netherlands, and Sweden, conservative financial practices have left business sectors better equipped to resume investment.

- Extent and timing of fiscal and monetary policies to stimulate recovery. The US is deploying $2.3 trillion in economic stabilization spending and $0.4 trillion in additional spending to support small businesses and healthcare providers. The US Federal Reserve and the European Central Bank slashed interest rates and announced major new lending programs for banks. Unfortunately, the US stabilization effort has had delays and bottlenecks in individual workers’ applications for unemployment benefits, Small Business Administration loans, and the $1,200 individual payment to those without recent US tax filings. In contrast, European countries such as Denmark, France, Germany, and the Netherlands had in place or have implemented policies to provide funds to businesses to keep workers employed and ramp up as consumers start shopping again. Countries like Italy and Spain have limited ability to increase their spending because of high debt loads and efforts to create Eurozone bonds.

Using these four variables, I have ranked the dozen largest economies (and tech markets) on their prospects for experiencing Scenario A or Scenario B. My rule of thumb is that countries that score higher than 3.5 on average across these variables have a 60% probability of experiencing Scenario A and a 35% probability of seeing Scenario B. Countries with a score of 3.5 face a 60% probability of Scenario B, a 30% probability of Scenario A, and a 10% probability of Scenario C. Readers can apply their own judgments and perhaps come up with different assessments. Remember, though, that the more countries that are in one scenario, the harder it will be for others to avoid the same scenario.