You Can’t Handle The (Consumer Personalization) Truth!

Covering the incredibly broad topic of consumer personalization means encountering a hodgepodge of client questions and terminology. In our new report The Truth About Consumer Personalization, we examine three common assumptions about personalization and convert them into three realities:

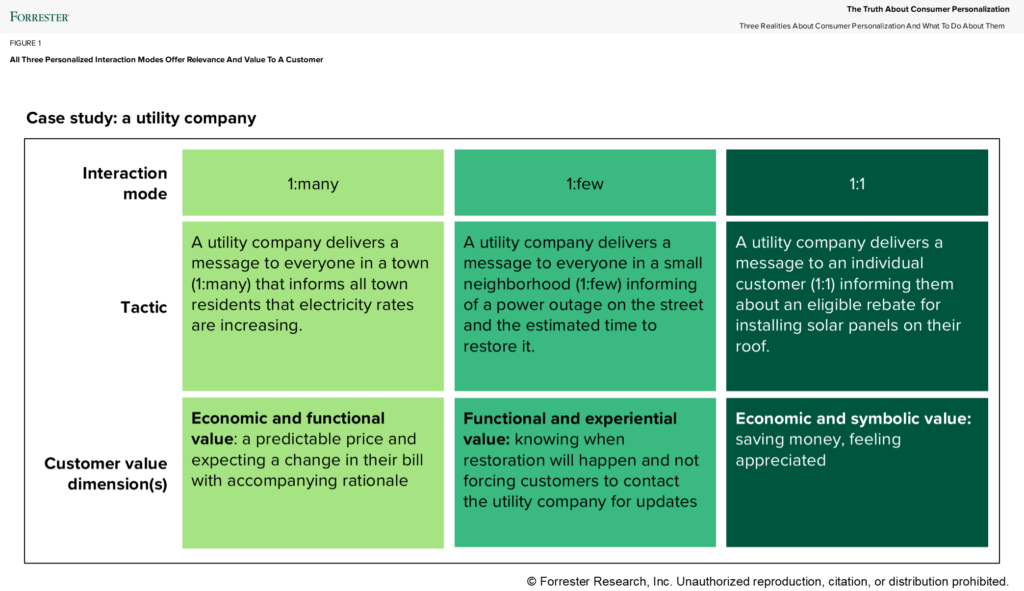

- Consumers don’t care about “hyperpersonalization.” This misguided term is one of my biggest pet peeves. Many organizations feel compelled to achieve this mythical ideal state. But consumers only care whether an interaction with a brand is relevant to them and if that interaction yields value for them — regardless of whether that interaction arrived via one-to-many, one-to-few, or one-to-one (see figure below).

- Context and customer are more important than content in a personalized moment. Contrary to the once famous statement, content is not king — context is. You can have hundreds of content variations, but if you don’t know why or who to engage with that content, does it matter? A personalized moment is comprised of context first and foremost, then the consumer/customer (the who), the content (the what), the touchpoint (the where), and the trigger (the when).

- Other companies aren’t a benchmark for personalization program performance. Organizations ask for benchmarks or “what good looks like in my industry” for personalization programs. Our answer: Measure against yourself. Personalization programs require experimenting and testing in the short term at the touchpoint level, medium term at the journey level, and long term at the relationship level to understand the impact of discrete personalization tactics, campaigns, and programs. It’s also critical to track both customer metrics (e.g., CSAT) and business metrics (e.g., interaction metrics).

A Deep Dive Into Additional Consumer Personalization Insights

Organizations must work hardest at reality number one (surrounding hyperpersonalization) because consumers and customers are the most important asset to a business and organizations struggle to strike a balance between customers’ goals and their own business goals. Start with a deep dive on understanding consumers’ and customers’ needs and attitudes toward personalized tactics.

Our anchor research on The State Of US Consumer Personalization, 2024 explained that people want personalized interactions that are 1) relevant to them and 2) valuable to them across four dimensions of customer value: economic, functional, experiential, and symbolic.

Our latest research, Understand Your Audience To Design Better Personalization Initiatives In 2025, dives deeper into consumers’ characteristics. We segmented consumers into two groups — “Personalization Receptives” and “Personalization Avoidants” — and highlighted differences between the two groups, such as:

- Younger urban consumers are more receptive to personalization tactics.

- Personalization Receptives feel more financial stress than Personalization Avoidants.

- Receptives build values- and trust-based connections with companies.

- Technologically adventurous consumers welcome personalized moments.

- Customer data privacy matters more to Receptives than Avoidants.

Understanding these characteristics allows organizations to be more thoughtful and deliberate when developing their personalization programs. For example, offering economic value with a personalized retail discount resonates more with Personalization Receptives who feel more financial stress, while emphasizing symbolic value with messaging about community belonging goes further with Personalization Receptives, who want more values- and trust-based connections with companies.

We’re here to chat about all things consumer personalization! Please schedule a guidance session or inquiry with us to continue the conversation.