Banks: Your Customers’ Cross-Channel Experiences Are Shoddy (Or Worse)

Note: If you’re a Forrester client, you can jump straight to the full report here.

The other day, I stopped by my bank’s ATM to get some cash. After entering my card and PIN and while waiting for my money (during which I was a captive audience), I was presented with an ad for a new service from the bank. Unfortunately, the ad’s call-to-action was a message telling me to call the bank’s 1-800 number to find out more.

I had just encountered one of the broken or inadequate cross-channel experiences that millions of customers face every year.

This is a lose-lose situation: In this case, the bank knew — or should have known — a heck of a lot about me as a customer, yet it failed to use context* to design a better experience and guide me seamlessly across touchpoints. And as a result, the bank also failed to cross-sell me any products or services.

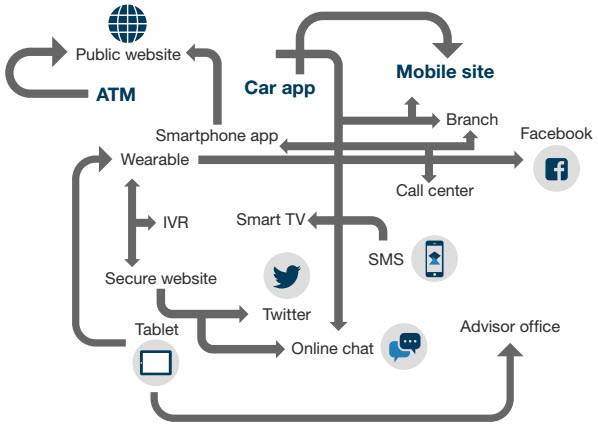

Forrester defines cross-channel behavior as any instance in which a customer or prospect moves from one touchpoint to another when completing an objective. Today, cross-channel goes way beyond online-to-offline transitions; going forward, these interactions will only increase in frequency and importance. Digital executives at banks are left with a tangle of customer journeys across various touchpoints (see image below).

In our new report, Design Better Cross-Channel Banking Journeys, we show that:

- Bank customers frequently move across touchpoints for sales and service. Among US online adults who researched and applied for a financial product in the past 12 months, more than half moved from one touchpoint to another during the shopping and purchase journey. This proportion varies a bit by market, but cross-touchpoint shopping is common across all developed countries. And this cross-touchpoint behavior continues once people become customers: 47% of US bank customers have had at least one cross-touchpoint banking interaction in the past 90 days.

- Too many of these cross-touchpoint experiences are either broken or bad. Many banks do a poor job of supporting cross-touchpoint journeys. For example, most banks do not offer branch appointment scheduling tools on their mobile apps or sites. Other cross-touchpoint transitions prove difficult, frustrating, unpleasant, and ultimately fruitless for customers. Secure websites, for example, often require customers to fill in form fields — like home address — that the bank should already know about the customer.

- Firms can gain competitive advantage by focusing on cross-channel design. Our report details the steps that executives and digital teams at banks should take to get ahead of customers’ cross-channel needs and expectations. The three main steps are identifying critical cross-touchpoint interactions; planning for customer journeys; and managing the transitions from one touchpoint to the next. Banks should focus on pairs of touchpoints, and they should appoint a multirole team that includes digital business executives, analytics experts, CX leaders, and business technology partners to lead their strategies.

I encourage you to read the full report here. Also, please share your thoughts in the comments section below.

*Forrester defines context as everything you know about a customer or prospect at the point of engagement.

Categories