The Consolidation Wars: M&A Is Rewriting Finance Automation

Coupa’s May 2026 acquisition of Rossum strengthens its accounts payable (AP) automation core and signals a deliberate move to anchor finance automation — built for the office of the CFO — in AI-powered platforms. By pairing Rossum’s large language model- and optical character recognition-driven invoice capture with its own strengths in payments, cash management, AP workflows, and spend visibility, Coupa fortifies its accounts payable position — and signals how central intelligent document processing has become to enterprise finance automation.

That is what makes the Rossum acquisition such a useful starting point for understanding the bigger market story. Over the past few years, M&A across accounts payable, accounts receivable, financial planning and analysis, financial close, tax, e-invoicing compliance, and spend management have steadily pulled the market away from fragmented point solutions and toward integrated CFO platforms. Strategic SaaS vendors, private equity firms, banks, and enterprise resource planning (ERP) providers are all chasing the same endgame: broader workflow coverage, stronger AI-driven automation, and greater control over the data and processes at the center of enterprise finance. For CFOs, the result is a narrower field of vendors offering wider capabilities, with clear gains in integration and automation as well as new concerns around choice, pricing power, and dependency.

Consolidation Is Reshaping The Finance Automation Market

Finance automation M&A has accelerated as vendors and investors pursue scale, scope, and embedded intelligence. There are four main types of M&A deals (see the figures below):

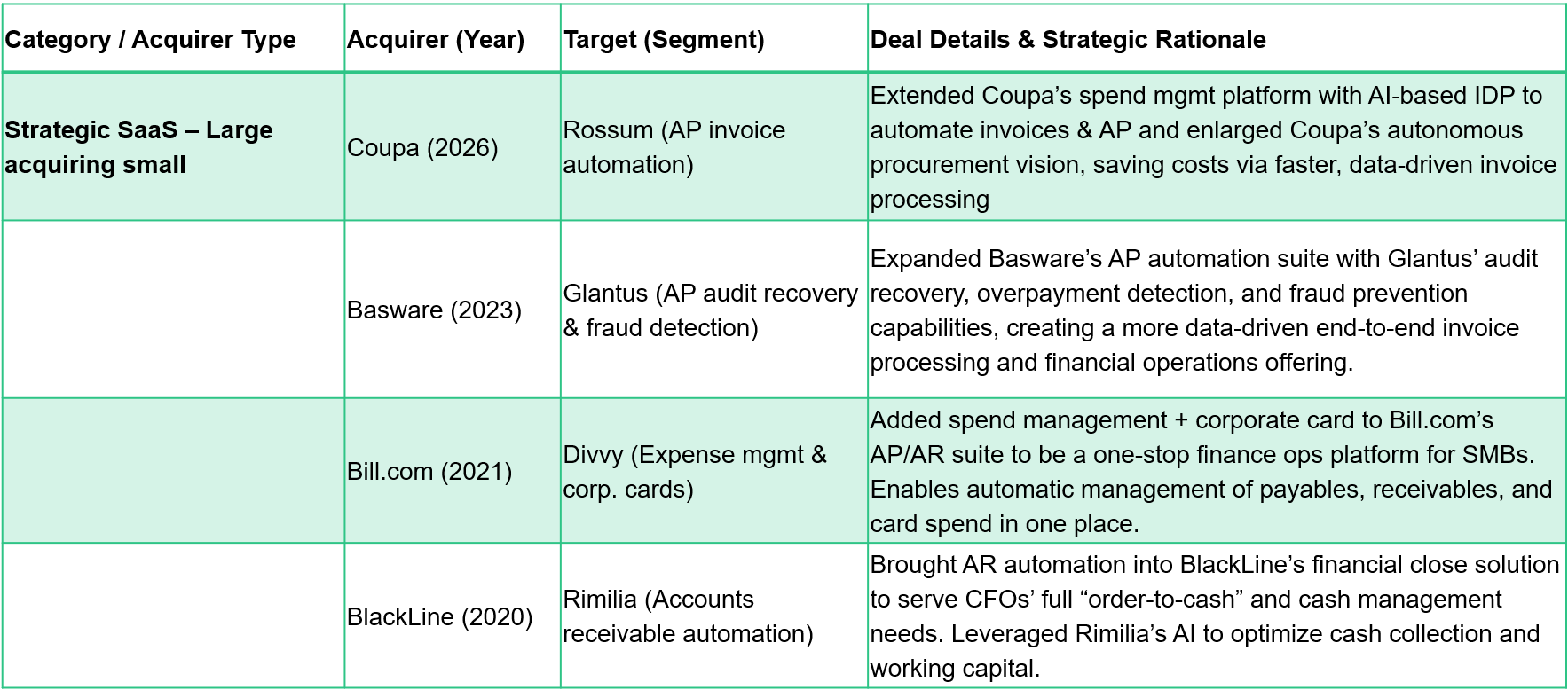

- Strategic SaaS vendors are buying deep capabilities. Large finance software providers are acquiring niche AP, accounts receivable (AR), and spend automation specialists to close portfolio gaps and speed time to market for advanced automation. Deals — such as Bill.com’s purchase of Divvy, BlackLine’s acquisition of Rimilia, and Coupa’s acquisition of Rossum — show how vendors are using M&A to embed AI‑driven invoice processing, spend management, and cash application directly into core CFO workflows. These acquisitions prioritize functional depth and workflow coverage over incremental customer growth.

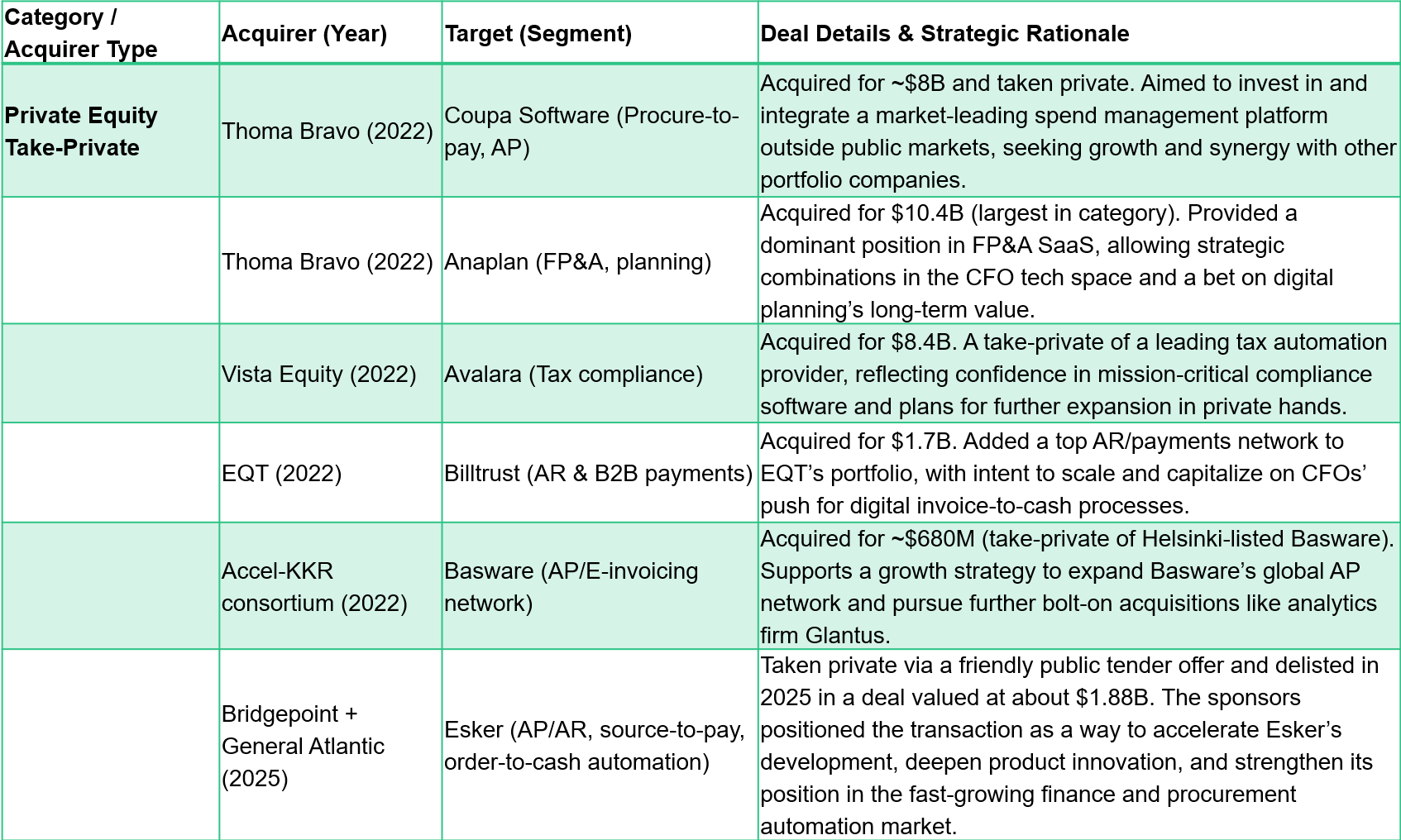

- Private equity is betting on durable CFO platforms. PE firms have taken multiple scaled finance automation leaders private — including Anaplan, Avalara, Basware, Billtrust, Coupa, and Esker. These firms attracted PE because of their recurring revenue, sticky workflows, and margin-expansion potential, reflecting confidence in the resilience of finance automation at the core of compliance-heavy enterprise processes. Under private ownership, these platforms are positioned to invest in integration, pursue bolt‑on acquisitions, and reduce short‑term market pressures while expanding horizontally across CFO use cases.

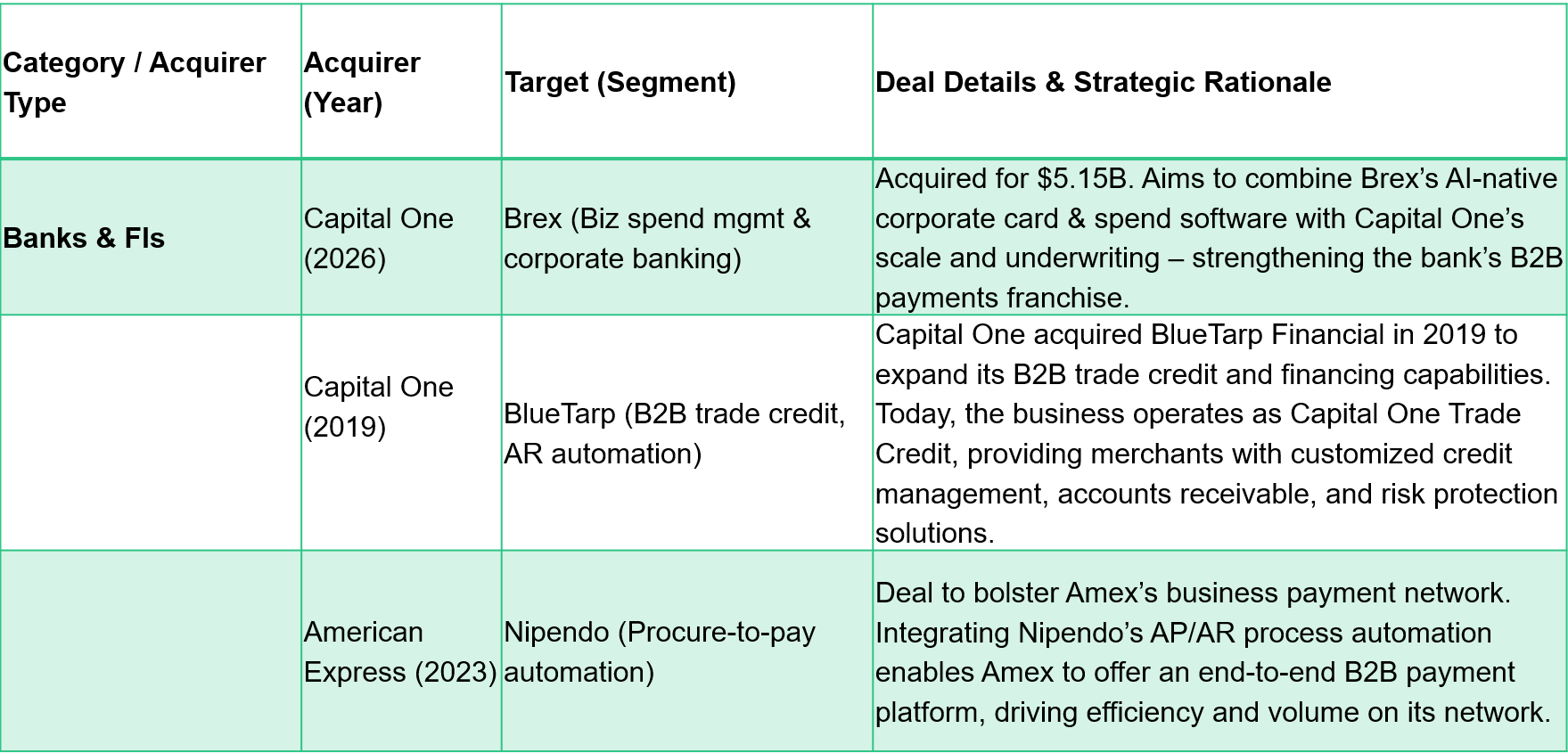

- Banks and card networks are moving up the software stack. Although historically partnership‑oriented, financial institutions have begun acquiring finance automation platforms outright. Capital One’s acquisitions of Brex and BlueTarp, as well as American Express’ purchase of Nipendo, demonstrate a shift toward owning the software layer that governs B2B payments, spend, and AP/AR. These moves reflect a strategic desire to control workflows, data, and the customer experience, rather than only payment rails.

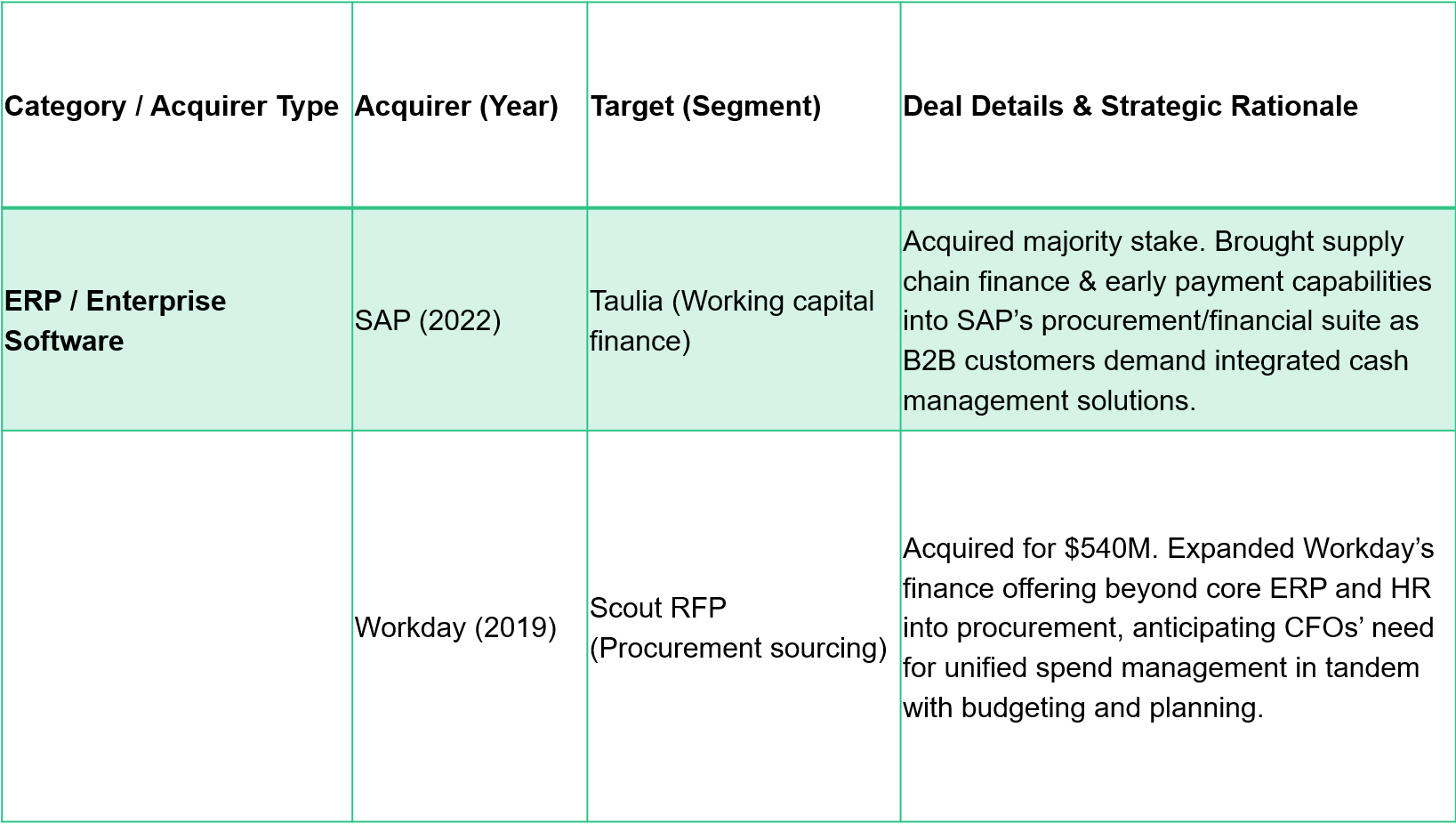

- ERP vendors are selectively filling finance automation gaps. ERP providers have pursued targeted acquisitions to extend finance capabilities without wholesale platform replacement. SAP’s majority stake in Taulia and Workday’s acquisitions of Adaptive Insights and Scout RFP illustrate how incumbents are embedding working capital management, planning, and procurement into existing suites. These deals help ERP vendors defend against best‑of‑breed SaaS competitors while meeting evolving CFO requirements. ERP vendors have slowed their acquisitions since 2019 — compared with the decade 2010–2019 — because they had already bought key finance automation assets. These vendors then shifted toward cloud-suite integration, embedded AI/automation, and partner ecosystems as valuations rose and niche finance workflows became harder to own end to end.

AI And Integration Are Primary M&A Catalysts

Across acquirer types, the strategic logic behind finance automation M&A converges on two themes: AI-driven automation and platform integration.

- AI‑driven automation is now table stakes. Acquirers consistently emphasize AI/ML, intelligent document processing, and AI‑native workflows as core deal drivers. Rossum’s data-capture LLM, Rimilia’s AR automation, and Brex’s AI‑native spend platform highlight how embedded intelligence has become central to value creation in finance software. Investors and strategists alike view AI as essential for eliminating manual work, improving accuracy, and enabling real‑time financial insights.

- Platform breadth outweighs best‑of‑breed depth. The dominant M&A pattern favors assembling broader platforms rather than maintaining isolated point solutions. Vendors are stitching together AP, AR, spend, financial planning, procurement, and financing to support end‑to‑end CFO workflows. This reflects customer demand for fewer vendors, unified data models, and integrated analytics — even if it means accepting less specialization in individual modules.

What This Means For Finance And Technology Leaders

Finance automation M&A over the past few years signals a decisive shift from fragmented tooling to integrated CFO platforms. For finance and technology leaders, the opportunity lies in leveraging deeper automation and integration, while the challenge is maintaining flexibility and control in an increasingly consolidated market.

- Expect fewer vendors with broader mandates. The finance automation landscape is concentrating around a smaller number of large platforms. This can simplify integration and vendor management, but it also reduces optionality and increases switching costs over time.

- Scrutinize post‑acquisition roadmaps and pricing power. Consolidation can accelerate innovation, but it can also introduce pricing changes, product rationalization, or shifting priorities. Finance leaders should assess how ownership changes affect long‑term product investment and commercial terms.

- Balance platform efficiency against dependency risk. Integrated CFO platforms promise efficiency, automation, and analytics at scale, but increased reliance on a single vendor heightens exposure to service disruptions, roadmap changes, and negotiation leverage. Multiyear technology planning should explicitly weigh these trade‑offs.

What To Read Next

Forrester has dedicated research in finance automation, including:

Top Agentic AI Use Cases For AP Automation In 2026

Total Economic Impact™ (TEI) Model For Finance Automation

The Finance Planning And Analysis Transformation Imperative

AI In Finance And Accounting — Wide-Eyed But Hopeful

Navigate The Accounts Receivable Automation Ecosystem

The Accounts Payable Invoice Automation Software Landscape, Q4 2025

Top AI Use Cases For Accounts Payable Automation In 2025

Top AI Use Cases For Accounts Receivable Automation In 2025

Forrester clients can set up an inquiry or guidance session to discuss this topic with me.