The State Of Sustainability In Asia Pacific: Regional Inconsistencies Hinder Real Progress

COVID-19 has put far greater emphasis on sustainability as a corporate social responsibility and business resiliency as a board-level priority. Globally, most firms now acknowledge the need to undertake climate action and improve their environmental sustainability performance.

But APAC firms are still very far apart in terms of what practices to implement and how aggressively to implement them. Government policies and positions are also wildly inconsistent, creating confusion and giving many firms cover to delay desperately needed action.

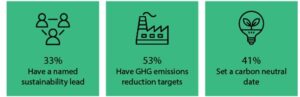

We analyzed the sustainability policies of a cross-section of large APAC firms to gauge the current state of sustainability efforts across the region. As part of this research, we reviewed publicly available information, including (where possible) the annual sustainability reports of 127 large companies in 12 key markets: Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Singapore, South Korea, Taiwan, and Thailand.

Given their size and environmental footprint, these firms’ policies will have the greatest near-term impact on climate action in the region. The good news is that a growing number of APAC firms are making public climate action and environmental sustainability commitments to reduce waste and energy usage and cut greenhouse gas (GHG) emissions.

The State Of Sustainability Among Large Firms In Asia Pacific

Unfortunately, too many firms’ sustainability plans remain limited, or in some cases simply performative. To make matters worse, many firms put these limited plans on hold during the pandemic. But this will change rapidly through 2022 as:

- Climate risks are growing and impossible to ignore. The extreme bushfires in Australia in late 2019 and early 2020 not only destroyed an area the size of Sri Lanka, but also released 715 million tons of carbon dioxide into the air. In July 2021, the central city of Zhengzhou, China was hit with a year’s worth of rain in just three days. Auckland International Airport’s analysis indicates that without direct climate action, the frequency and intensity of flooding will impact its ability to continuously operate by 2090.

- Customers and employees expect action. The pandemic has driven a rise in the prevalence and intensity of values-based consumers who are rethinking their priorities, focusing more on the environment, and beginning to pressure brands to take action. This also applies to employees, who increasingly factor corporate values into decisions on which companies to work for.

- Investor pressure, and opportunities, are growing sharply. As the pressure to embrace sustainability mounts for firms, institutional investors have emerged as enablers via sustainable finance and as gatekeepers by monitoring the environmental, social, and governance (ESG) credentials of the investments under management. To spur sustainable investments, countries including India, Malaysia, and Thailand published guidance on ESG guidelines and reporting. Hong Kong and Singapore are going further, racing to establish themselves as regional hubs for sustainable finance.

- Government incentives evolve into mandates. Climate-related legislation varies widely across the region. ESG regulations, for instance, remain fragmented, and unlike the European Union, there are currently no regional ESG disclosure frameworks in Asia Pacific. But this is set to change. New Zealand is the first country in the world to enact a law forcing financial services firms to assess the effects of climate change on their own investments as well as companies they lend money to. Singapore’s efforts to reduce the release of hydrofluorocarbons has quickly expanded from grants encouraging alternative approaches to regulations forcing compliance.

This blog post is part of Forrester’s COP26 series. For more Forrester insights on sustainability, see the full set of Forrester’s climate action blogs.

Categories