Is The Sales Tech Party Over?

Back To The Roaring Twenties

It wasn’t supposed to be like this. Early in 2021 the media was filled with talk that we would see a return to the Roaring Twenties, those golden years of economic prosperity before the first great Wall Street crash in 1929. And while socially, the episodic nature of COVID-19 may have slowed our roll back to the good times somewhat, tech investment certainly came roaring back. In fact, it was more like a tsunami of investment as VCs and private equity surfed a wave of available capital and low interest rates to drive record levels of funding and valuations. In 2021, US$630 billion of investment piled into VC-backed companies, double the amount in 2020. Sales tech got in on the good times as well, as investment rose dramatically from US$1.8 billion in 2020 to over US$4.3 billion in 2021 with over US$3.7 billion of that amount going to late-stage funding rounds (Source: Venture Scanner – data accessed on June 17, 2022).

Source: Crunchbase

The End Of The Era Of Easy Money

However, just a few months later it feels like the party that was supposed to last a decade is already done, and everyone, including the sales tech industry, is facing a new reality. The era of easy money is over. Central banks kept interest rates at zero, making it easy for companies to borrow debt. Investors encouraged their portfolio companies to rapidly scale to drive a dominant market share, feeding a culture of high cash burn. Such dynamics drove high valuations across tech. While the risk of some businesses never becoming profitable was real, continued access to low-cost financing meant that any day of reckoning was pushed way down the road.

As this investment-friendly climate changes, it brings significant implications for both investors and providers. Those tailwinds of easy money at low cost have now become headwinds for the tech industry. A perfect storm of macroeconomic and political factors (war in Ukraine, the COVID lockdown in China, among others) has driven up commodity prices and inflation while constraining market liquidity.

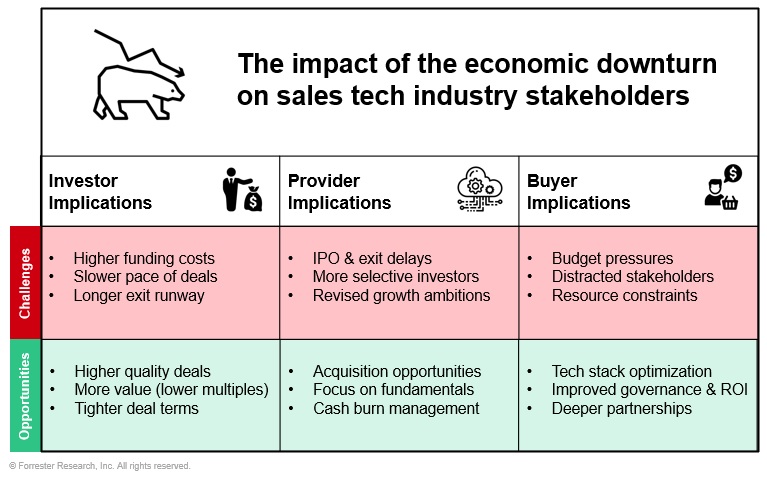

The Implications For Investors In Sales Tech

- Challenges for investors. Although VC and private equity (PE) funding mechanisms work differently, as the cost of borrowing rises and market conditions worsen, both sources of funding have slowed. In discussions with both VC and PE funds, fund managers are become pickier on where they invest, at what stage, and how. There is a renewed focus on risk reduction and ensuring that multiples paid are in line with the new reality and the fact that their exit schedule has been extended. In such a climate, the bold long-term vision frequently espoused by startup founders quickly becomes less interesting than the potential pathway to profitability and free cash flow.

- Opportunities for investors. Investment terms (the get for the give — e.g., liquidation preferences, the ability to block sales, board seats, etc.) are tightening as the volume of investment deals declines and competition between funds for deals decreases, giving investors increased influence in their portfolio companies. The changing environment doesn’t mean investors have stopped looking for great companies to invest in; there remains a significant amount of “dry powder” to be put to work, but inevitably investors are going to be more selective. Valuations and fundamentals will be scrutinized to a far greater degree given the increased risk, cost of funding, and expanded timeline for exit.

The Implications For Providers In Sales Tech

- Challenges for providers. The coming months will likely bring a more challenging period overall for sales tech providers. They not only face greater funding challenges in the private markets (where almost all sales tech providers exist) but may at some point face a potential tightening of demand for their products and services as their B2B clients and prospects (many of whom are also in tech) face the same changing market conditions. Finding and converting deals may take longer while pricing pressure would further constrain growth and profitability. Sales tech providers at all stages will have to reset expectations on growth with a new focus on scaling at a reasonable cost. That inevitably means a tightening of operating costs, with sales and marketing spend and headcount facing pressure in the coming months as startups look to extend their cash runway to 18 to 24 months, when hopefully the climate for funding and public offerings becomes more positive. Right across sales tech from seed to late-stage, valuations are likely to come under pressure. Early- and midstage companies in particular face a dual struggle of finding the next funding round and avoiding a down round along with the associated dilution that comes with it. The pressure of staying liquid while continuing to acquire and retain customers will force some smaller providers to rethink their longer-term strategies, as some founders may have to consider the harsh reality of exit in the form of M&A or private equity purchase. Depending on the level of cash burn, the fundamentals of the business and their agility in their go-to-market execution, those decision points may come sooner rather than later for some companies.

- Opportunities for providers. Despite understandable disappointment (mostly unspoken) among many late-stage sales tech providers that macro conditions have contrived to close the opportunity for IPO for now, these companies are quickly pivoting to face the new reality. Experienced leadership teams with significant cash on hand (thanks to large late-stage funding rounds last year) can balance the extension of their cash runway while picking up some discount acquisitions that may previously have been unavailable to broaden their platform and market value. Disciplined cost and cash management will be key as will a continued focus on performance fundamentals (MRR, retention, etc.). This quarter, we’ve seen both Mediafly and Clari extend their platforms with the acquisitions of ExecVision and Wingman. Both deals demonstrate PE and VC confidence in the continued expansion of sales tech platforms like these, and we expect to see more M&A activity in the second half of the year.

The Implications For Buyers Of Sales Tech

- Challenges for buyers. Whether public or private, B2B companies across most segments are going to face increasing top and bottom-line challenges. This will place pressure on tech investment across sales and marketing. Owners of tech in these functions must demonstrate internally the value and ROI of such investment as they seek to expand the use and adoption of technology in organizations where both leadership and sales teams may be increasingly distracted by revenue concerns.

- Opportunities for buyers. In response, now is the time for those with ownership of revenue or sales tech stacks to consider the maturity of their tech management. It’s time to consider how to organize to optimize tech, to manage implementations and drive organizational readiness and adoption. They must demonstrate a structured, thoughtful, but ruthless approach to tech stack optimization. The pressure for such change may vary depending on organizational scale and external impacts, but given the variance in adoption and functionality value across these tools, operations teams need to proactively start assessing and optimizing their tech portfolios.

Despite More Challenging Conditions, Demand For Sales Tech Will Remain Strong

While conditions may be changing, the digital transformation of sales won’t go backward, and Forrester sees little evidence at this point that the demand for technologies that optimize sales performance is falling off. Based on our experience, tougher times will force B2B organizations to lean harder into driving improvements as they seek to maximize customer relationships, do more with less, and rigorously manage revenue.

From a provider perspective, 2022 has already shown that providers that can demonstrate differentiated value can still attract significant investment. Invoca, a platform that uses AI to analyze calls for marketing, sales, and customer agent training purposes, just closed an $83 million funding round on June 14, and we expect other well-funded providers to continue with modest acquisitions throughout the year. Providers that communicate a clear and obvious value proposition, are adaptive, and can consistently solve persistent go-to-market challenges for B2B sales organizations remain well-positioned to grow. More broadly across sales tech, we expect the two primary trends of consolidation (of providers) and convergence (of functionality) to continue and accelerate in this changing environment.