Banking Functionality Doesn’t Differentiate Banking Software Anymore, But Technology And Ecosystems Do

Today’s banks need to offer better customer experience — still only “OK” in many geographies and deteriorating in the US. But this isn’t enough to remain successful: Growing regulatory requirements, the rise of banking ecosystems and embedded finance, and the rapidly changing banking landscape demand future fit technology. Both business and technology leaders in banks are aware that their often aged banking platforms do not provide a great foundation for adaptiveness, creativity, and resilience and are investing to change this. Forrester’s 2022 data shows that 73% of business and technology professionals at financial services firms say their organization plans to maintain or increase their investments in core banking applications over the next 12 months. But they are doing so against cost pressures caused by the pandemic, the rapidly deteriorating economic climate, and, increasingly, environmental, social, and governance (ESG)-related business risk.

In this demanding environment, technology teams in banks typically look for state-of-the-art digital banking processing platforms (DBPPs) that comprise functionality such as agile core banking and further banking-specific back-end software. If you’re interested in leading DBPPs in retail and corporate banking, please have a look at the related Forrester Wave™ evaluations. But what did we learn during the evaluations? While selecting the best-suited solution for their bank, technology teams need to be aware that:

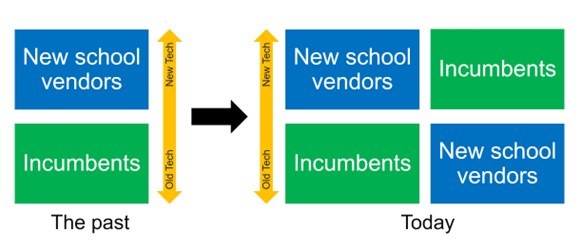

- Technology and architecture aren’t the dividers between incumbent and new-school vendors anymore. The earliest new-school vendor started to revolutionize how banking software gets delivered more than a decade ago. At that time, we could observe a clear separation: New-school vendors used new technologies and architectures; incumbent vendors did not. Today, the situation is different. Many incumbent DBPP vendors have invested heavily in moving to entirely new architectures, while some new-school players are updating their solution architectures only now. But don’t get me wrong — you will still find some pretty monolithic solutions in the incumbents’ camp.

- Functionality in retail and corporate banking is no longer a differentiator. Incumbent vendors have spent decades building broad and rich banking functionality. New-school vendors typically started with core banking about a decade ago and have enhanced their solutions’ business capabilities over time. The historical functional differences between leading members of each group are diminishing (unless you’re comparing business requirements and functionality at a very detailed level). New differentiators, however, such as ESG-related functionality, have come into existence.

- Ecosystems and partnerships increase agility and broaden functionality. Today’s new-school vendors need to use partner ecosystems to add functionality to their solutions’ environment. These ecosystems also allow banks to switch to better-suited solutions available within a given ecosystem. Ecosystem and partnership-based approaches are not exclusive to new-school players, however; incumbents work with both organic functional enhancements or functionality from partners, and leading incumbents think about automated marketplaces that help banks swiftly and seamlessly introduce new capabilities to enrich their own DBPPs.

For more guidance on navigating the changes ahead, please reach out to schedule an inquiry here. Not yet a Forrester client? Get in touch.

Related Forrester Content

- The Forrester Wave™: Digital Banking Processing Platforms For Corporate Banking, Q3 2022

- The Forrester Wave™: Digital Banking Processing Platforms For Retail Banking, Q3 2022

- Now Tech: Digital Banking Processing Platforms (Corporate Banking), Q1 2022

- Now Tech: Digital Banking Processing Platforms (Retail Banking), Q1 2022