How To Build A Premium Airline In The Sky Of Sameness

Budget Is Dead. Long Live Premium?

The demise of Spirit Airlines has provided endless fodder for late-night comedy that pokes fun at the misery of budget airline travel in the United States. But what about the other end of the spectrum? Do legacy carriers merely move people through the sky, or can they lay claim to a premium offering that genuinely earns preference and loyalty among flyers?

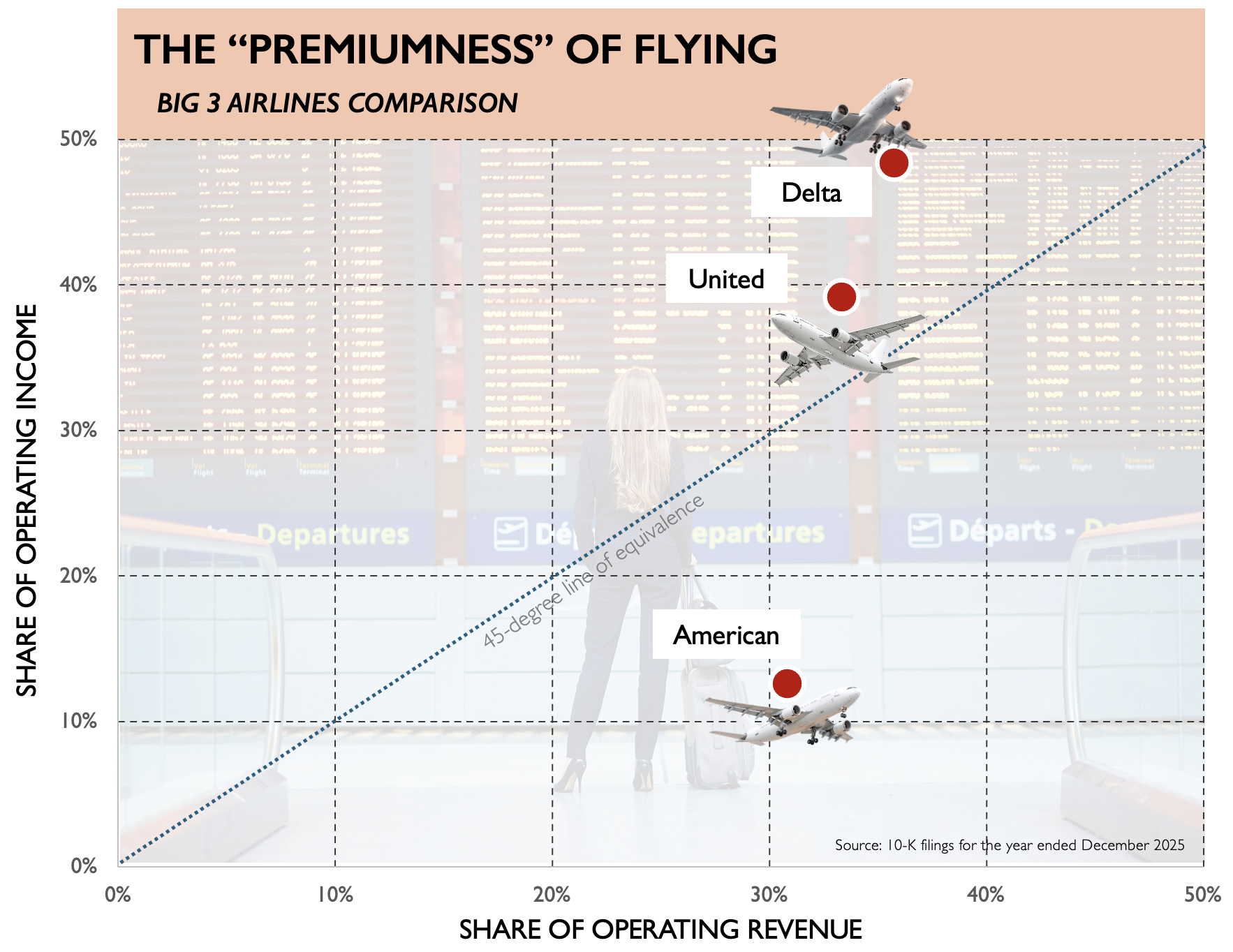

A proxy for premiumness is a company’s ability to command a price premium. One quick test is to compare a company’s share of category revenue with its share of category profit. I ran a back-of-the-envelope analysis of the top three US carriers, and the results are stark (see the chart below):

- Delta, United, and American each account for roughly a third of their combined operating revenue — they occupy similar positions on the horizontal axis.

- But the three diverge sharply in income share — they occupy very different positions along the vertical axis:

- Delta, accounting for about a third of revenue, captures nearly half of the combined operating income.

- United’s income share also exceeds its revenue share, placing it just north of the 45-degree line of equivalence, but not as much as Delta’s.

- At the other end of the spectrum, American captures only 13% of the operating income among the three — a glaring disparity in the wrong direction.

Differentiated Premiumness

Delta’s premium offering is fueling its growth — in Q1, premium revenue grew 14% year over year, while main cabin grew just 1%. Delta’s premium strategy is about precision. The airline is relentlessly focused on the passengers who matter most to its bottom line: those who fly in the nose rather than the tail, stop by Sky Clubs for a preflight martini, and charge their black cars to American Express Delta Reserve cards.

As for the rest of us? Even if Delta’s TLC is disproportionately reserved for its most valuable customers, a rising tide still lifts even the sardines packed together in coach. Free Wi-Fi, seatback entertainment, and a better app benefit every flyer.

But in other ways — especially as low-cost carriers disappear — it may become a race to the bottom. In the wake of Spirit’s demise, Delta eliminated food and beverage service on flights shorter than 350 miles. Yet Delta’s strategy is one of precise premiumness. If you happen to be in first class on your short hop from Cincinnati to Detroit, you can still enjoy all the hazy IPA your half hour in the air allows.

What is especially remarkable about what Delta has achieved is that it is not a niche premium offering catering to a small focus segment in exchange for high-price premiums (think Neiman Marcus versus Macy’s). Rather, it’s a mass-market brand with the dominant market share among its legacy peers, yet it successfully differentiates to offer a premium service and justify a premium price.

How To Build A Premium Brand In Commodity And Depressed Markets

Even in today’s environment of rock-bottom consumer sentiment, there remains a clear opportunity to grow with a premium product — and not merely by catering to the 1% driving Bentleys while draped in Bulgari. There is a vast middle willing to pay a premium for something sufficiently differentiated to justify the privilege. The companies that succeed will not rely on a generalized understanding of customer needs; they will deploy finely tuned strategies rooted in precision.

To learn more about how to be precise in your premium and customer strategy, read my latest report: Down But Not Out: Growth Strategies For The Pessimism Economy.

———————————————————————————————————————

Follow my research: Go to my Forrester bio and click “Follow.”

Chat with me: If you’re a Forrester client interested in discussing these topics, please schedule time with me for an inquiry or a guidance session.

Plan a session: If you’re a Forrester client looking to host a strategy session on a related topic, please contact your account team or email me at dchatterjee@forrester.com.