Simplicity Underpins Future Payment Fabric And The Future Of Payments

Welcome to payment fabric — Forrester’s perspective on the future of payments. We live in a world where centuries of glacial paper-based payments evolution have given way to exponential digital payment innovation: a world of fragmentation across device, form factor, and payment method. Against this backdrop, regulators struggle to contain risk, and firms struggle to meet the changing needs of consumers. Something has to give.

We Have Passed Peak Payments — The Next Challenge Is Simplification

Increasingly blurred boundaries mean that practically anyone can declare themselves a payment provider, using banking-as-a-service to embed payments. Customers can filter this choice through a lens of preference and habit. For firms, complexity is only increasing, as they try to reconcile the demands of customers with the plethora of capabilities from payments providers and networks.

To build our future vision, we spoke to leaders from across the world of payments and distilled their insights into a few bold themes to help tomorrow’s leaders make sense of this complex and fast-changing environment. We heard one thing loud and clear: Future payment fabric providers must present complexity in a simplified form.

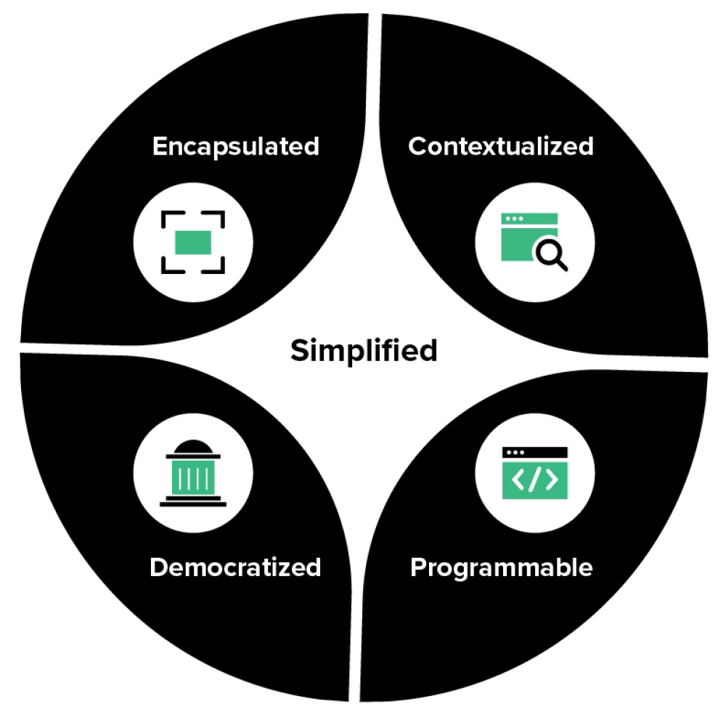

Four future fit themes manifest around this quest for simplification.

Payments Will Be Encapsulated, Contextualized, Democratized, And Programmable

Firms will need more agility to be future fit and cope with complexity, and many will turn to payment fabric providers that abstract complexity away from their processes and their customers.

Future payment fabric will be:

- Encapsulated. Today’s embedded finance becomes encapsulated payment technology to wrap value around a payment and distribute it to the point of need. Enriched data will live with the payment, offering transparency, automation, reconciliation, and attribution for multiparty payments and loyalty and triggering micropayments when a process reports a change in state. Simplified payment components will put checkout and authorization optimization under firms’ control.

- Contextualized. Contextual authentication — behavioral biometrics, geolocation, device fingerprinting, localized AI rules — and decentralized digital identity will offer consistent authorization with minimal customer intervention. Payments providers will offer “in a box” solutions, wrapping value-added services into bespoke platform solutions designed for an industry or scenario. Control of a payment may reside with the payment itself, the device, the component, or be managed remotely.

- Democratized. Digital payments will not supplant prior form factors unless they support all customers and can be translated to low-tech environments. Regulators will insist on this and on lowering the cost of entry through open finance and interoperability to migrate underbanked populations toward financial services. Digital payments offer inclusivity, while central bank digital currencies (CBDCs) and smart payments provide a means for governments to distribute funds. Payments must be affordable to all and to the planet.

- Programmable. Payments themselves will come equipped with their own rules of engagement. Programmable money will use tokenized payments that set the conditions of operation, restricting service to a merchant, a value, a location, or a time in device-agnostic payment payloads. Programmable payments will enable autonomous machine-to-machine transfers and settlement, with digital currencies such as stablecoins or CBDCs or on-device ledgers.

In The Decade Ahead, The Focus Of Payments Innovation Shifts From Consumers To Businesses

If the last decade was all about consumers and mobile payments, the next belongs to businesses and autonomous payments in connected devices. Forget embedded payments — the story becomes one of embedded payment technology, as today’s fragmentation gives way to orchestration and re-bundling and successful payment firms offset complexity with scenario-based solutions.

We will continue to see individual fintechs unbundle valuable services from payments; future payment leaders, however, will shift their strategy to focus on reassembling capabilities and services to offer both horizontal and vertical solutions that specialize and simplify. We will see both horizontal aggregators and orchestrators above and between payment layers, as well as vertically focused integrators and re-bundlers that specialize in an industry segment. These payment-as-a-service providers, aggregators, and orchestrators must also anchor value around payments — for customers, firms, devices, and developers — to differentiate and avoid becoming a commodity.

We Are Moving Into An Era Of Greater Control Over Payments

Event-driven payments, decentralized enablement of rules, and transparent traceability pepper the future, as vehicles become connected devices with embedded ledgers and capable of autonomous transactions. This era will be one where scale matters, as platforms build their own payments networks and networks create their own interoperable consortia. P27 and the European Payments Initiative are just the start of an age of interoperable open finance.

If you’d like to learn more, please take a look at our new research on the future of payments. Do reach out if you have any questions or would like to know how we can help you and your firm prepare for the future of banking.

Related Forrester Content

- The Future Of Payments

- Predictions 2022: Payments

- Demystifying Payment Tokens

- Now Tech: Enterprise Payment Processing Platforms, Q3 2021

- Demystifying Stablecoins: They Can Have An Important Role In The Financial System If They’re Designed And Governed Appropriately

- Cryptocurrency: Everything Retailers Need To Know

Categories

- Architecture & Technology Strategy

- B2B CX

- Banking

- CIO insights

- Core Tech Strategy

- customer experience

- customer loyalty

- customer obsession

- customer-centric design

- digital business

- Digital Transformation

- Emerging Technology

- financial services

- fintech

- Retail Trends

- store of the future

- technology-driven innovation